- Fintechs’ and non-banks’ market share of SME lending is growing significantly

- Banks are fighting back with more flexible funding solutions, cash management services, and digital service initiatives

- Partnerships, analytics, and value-added services are core to banks’ new offerings

In countries around the world, challenger banks and fintechs are launching innovative solutions that are starting to take SME banking business away from traditional banks. In the US, for instance, Kabbage has enabled more than 170,000 SMEs to gain access to more than $6 billion in working capital. Volt Bank in Australia just received a banking license and will soon start to deliver faster and more personalised services, at a time when an inquiry by a Royal Commission exposed malfeasance that has led to trust in banks plummeting. And start-ups in Southeast Asia such as Funding Societies offer P2P lending, with volumes so far exceeding $2 billion, that reaches SMEs that are largely untouched by banks.

Challenger Banks Fill a Gap

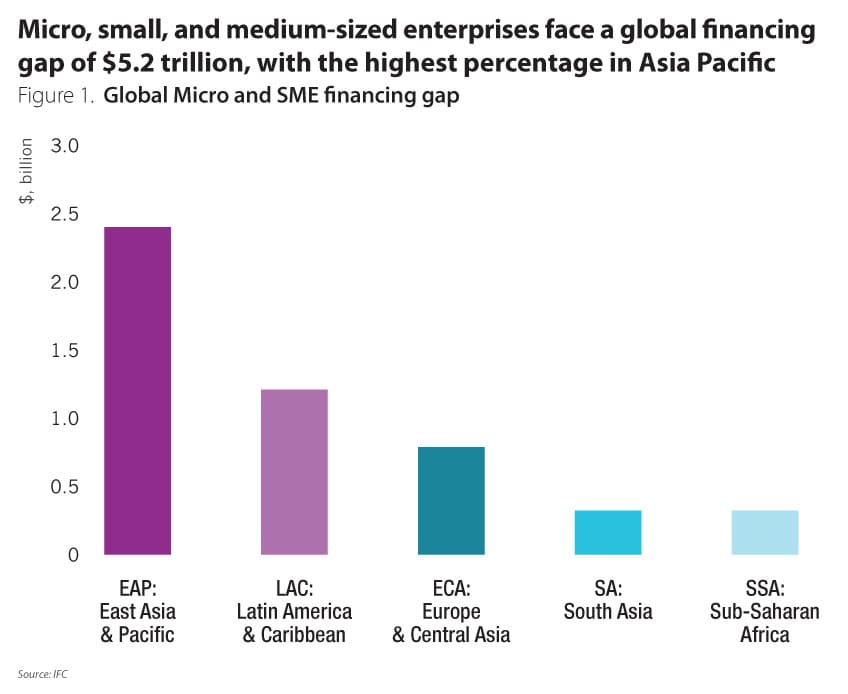

There is clearly a need for the services fintechs and challenger banks are providing. The IFC estimates that SMEs face a funding gap of $5.2 trillion globally, of which $2.4 trillion is in Asia alone, and 65 million MSMEs are credit-constrained.

Micro, small, and medium-sized enterprises face a global financing gap of $5.2 trillion, with the highest percentage in Asia Pacific

Figure 1: Global Micro and SME financing gap

Source: IFC

In Australia, 96% of SMEs face funding issues naming onerous loan conditions, having to provide property security, loan inflexibilities, and short loan tenures as their major concerns, according to the Scottish Pacific SME Growth Index. Currently, less than 20% of SMEs pick their bank as their main source of lending capital. The survey also found businesses were about as likely to turn to an alternative lender as they were to ask their bank for a loan, and predicted by 2020 alternative lenders were likely to overtake traditional lenders as key funders of small businesses.

Moreover, the ADB estimates that SMEs in Asia face annual trade financing gaps of $150 billion, and 60% of companies rejected for trade finance did not proceed with the trade because of the lack of funding.

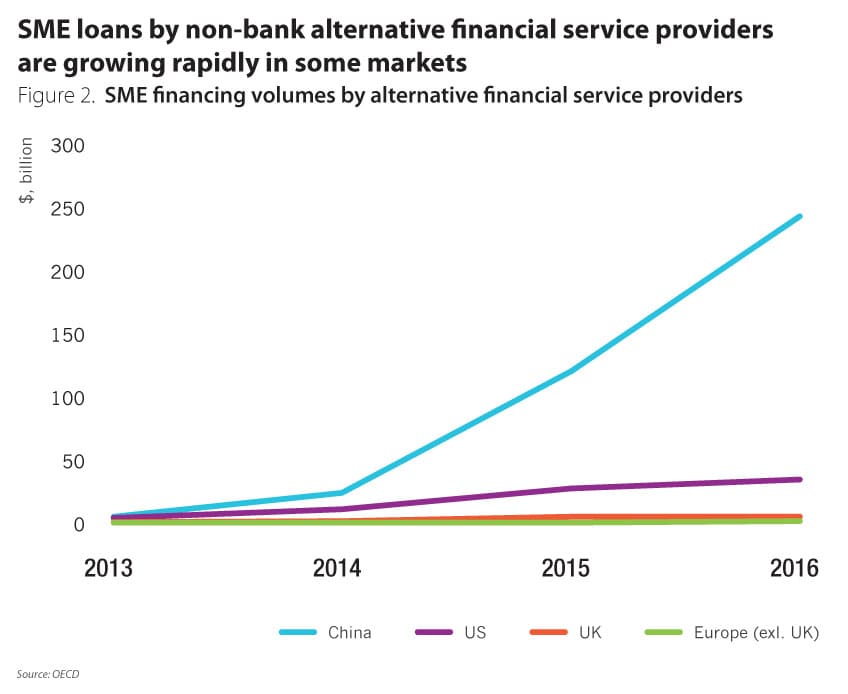

As a result, online peer-to-peer lending and equity crowdfunding for businesses increased significantly in 2017 albeit from a low base, especially in countries with small markets, based on the latest OECD SME and Entrepreneurship Finance report. China, the United Kingdom, and the United States continued to have the biggest online alternative finance markets for businesses. Volumes are increasing significantly in some markets.

SME loans by non-bank alternative financial service providers are growing rapidly in some markets

Figure 2: SME financing volumes by alternative financial service providers

Source: OECD

Fintechs and challenger banks such as Mybank, Tide, Penta, Ideabank, Iwoca, and Kabbage, for instance, deliver attractive value propositions for SMEs in markets in Europe, US, and China that significantly affect traditional banks. Those alternative lenders understand their customers’ need for a frictionless customer experience and have built credit journeys that align to business expectations. The speed, transparency, agility and convenience these new players offer are leading to better products, processes, and customer relationships.

They also are changing the game in charging fees. For instance, banks offer business current accounts free for an initial trial period but will start charging after, often requiring a minimum deposit balance. While not all banks impose charges on SMEs, annual fee charges can range between $30 to $100 in the Asia Pacific. Some challenger banks heavily exploit those multiverses of fees and lack of transparencies. Tide, a UK-based SME-only neo-bank offers no monthly fees and transaction are instantly connected to accounting software. The bank, which has around 65,000 members in the UK translating into a 1.14% share of the market which totals 5.7 million UK SMEs, introduced a multi business account where SMEs can access up to five businesses on the same Tide app, switching between them.

Mybank, Ant Financial’s online commercial bank, grew from its inception in 2015 to April 2019 to 16 million micro and small businesses who manage their entire accounts, from payments to loans and insurances via mobile app. According to a Reuters’ article in February 2018, the company said the cost of approving a no deposit and no collateral based small business loan can be as little as $0.3 (2 RMB), compared to at least $318 (2,000 RMB) at a traditional Chinese lender. It also stated that it incurs a cost of fund of 5% to 6%, and a net interest margin of 3% to 5%. Its core is 100% cloud-based.

In the UK, Ebury provides supply chain financing and foreign exchange services for more than 24,000 SMEs, which have taken advantage of its support for international payments and flexible financing, Ebury has transacted foreign exchange trading of more than $16 billion (£12.5 billion) to support the firms.

Iwoca, Europe’s second largest alternative lender, provides fast and flexible financing to SMEs trading in the UK, Poland, and Germany via an automated lending platform and has made loans to 25,000 SMEs totalling almost $1 billion (£800 million) since 2012. According to Q4 2018 data provided by UK Finance, the lender has overtaken Santander and HSBC for the first time in regards to small business overdraft approvals and moving its market share from 10% to 12% on a quarter by quarter comparison. The company says it aims to fund 100,000 SMEs in the next five years. The number of overdraft facilities offered by the UK banks to SMEs has declined by 50% since 2011.

In the US, PayPal is now one of the top five lenders for SMEs and sees banks such as Bank of America and J.P. Morgan Chase as peers. Tech companies are getting into the market too, with Intuit recently launching QuickBooks Capital to provide funding with credit analysis based data from QuickBooks and other sources.

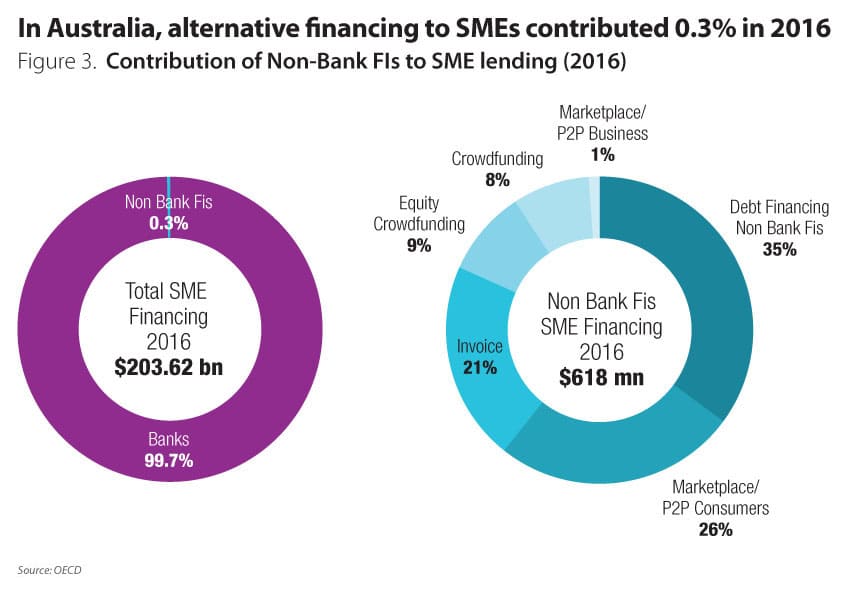

In Australia, alternative financing to SMEs contributed 0.3% in 2016

Figure 3: Contribution of Non-Bank FIs to SME lending (2016)

Source: OECD

Most alternative lenders still demonstrate poor financials

One of the key weaknesses of alternative SME lenders is the misalignment of product offerings and channels to the target customer segment. A misfit on the product side leads often to low take up. On the other hand, players do not scale if channels are not aligned with the customers. This ultimately impacts financials. Most SME financing platforms such as Lending Club in the UK are incurring losses because they may have not managed the scientific data part driving the business or are insufficiently automated in particular on the underwriting side. Excluding those large players in the SME space, the small number of cases underwritten is often insufficient for machine learning as well. This is based on a lack of SME customer data to create useful algorithms for automated decision-making, unless one can rely on large pre-existing transaction platforms such as Mybank or Webank in China.

Traditional banks are getting better in servicing SME’s

In most countries, traditional banks still dominate the market for SME banking, at least for now. Eight out of 10 SME loan applications were approved by banks in the third quarter of 2018, according to the latest figures from trade association UK Finance, because SMEs continue to trust their brand and reputation, even though small businesses face servicing challenges and lack personalised services.

To keep this market-leading position, leading banks are developing innovative solutions through partnerships, analytics and enhanced services.

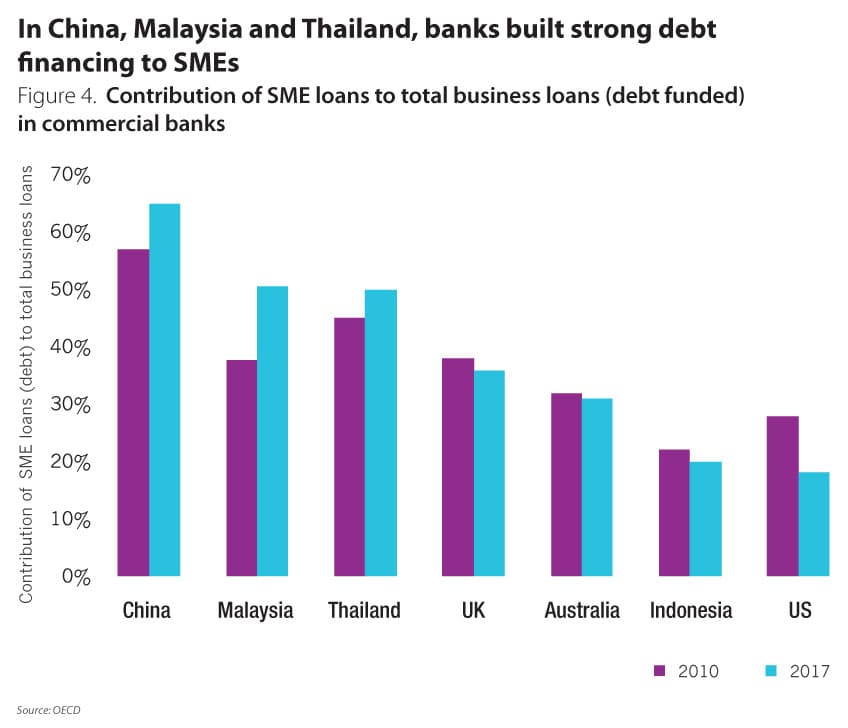

In China, Malaysia and Thailand, banks built strong debt financing to SMEs

Figure 4: Contribution of SME loans to total business loans (debt funded) in commercial banks

Source: OECD

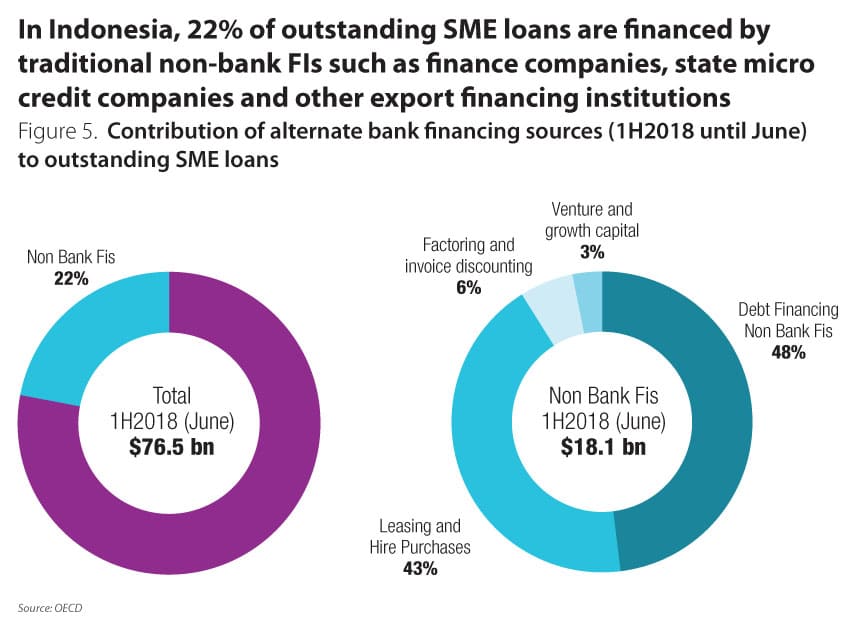

In Indonesia, 22% of outstanding SME loans are financed by traditional non-bank FIs such as finance companies, state micro credit companies and other export financing institutions

Figure 5: Contribution of alternate bank financing sources (1H2018 until June) to outstanding SME loans

Source: OECD

Capital Funding and Cash Management

One common challenge businesses face is the timely collection of payments from their customers. Besides digital collection solutions, a bank in Singapore launched a business revolving term loan catering to short-term working capital needs. It offers businesses a flexible short-term loan and overdraft combined. Businesses can draw, repay and redraw any number of times at their convenience, with no penalty for full repayment before the loan matures. NAB Australia approves currently around 80% of SME loans within 24 hours. Banks have also built a comprehensive suite of alternative funding and business solutions for SMEs at every stage of their business.

Payroll remains another key administrative task for many SMEs, in particular in country with large unbanked populations. A foreign bank in Indonesia launched a bulk payment solution in the form of an e-Wallet with DOKU, Indonesia's largest and fastest growing provider of e-payment solutions. Disbursements can be made within two hours.

For domestic and cross-border payment needs, the application of segment usage patterns can identify high volume customers to provide free bundle of monthly transactions, as well as simplified digital monitoring of their domestic and cross border funds. For cross border payments, just as tracking a courier package in transit, banks provide greater visibility of where the money travels, what fees have been deducted by overseas banks or when payment has been received by the recipient.

Digitising the Platform

While digitisation is fundamental for fintechs’ services, banks have taken longer to digitise their platforms which translates, among else, into longer turnaround times.

On average SMEs in emerging markets such as Indonesia and the Philippines have to wait between three to five working days to obtain a physical cheque book, while turnaround for standard SME loans can take between 10 to 15 working days for small business loans which includes collateral appraisal and credit investigation. Often however, loan recommendations go through review committees which can extend this process to 30 to 45 working days.

Now, though, leading banks are digitising back-end processes, tools for frontline staff and customer interfaces to make SME banking faster and easier.

Digitisation and robotic process automation in the back office have reduced paper, increased speed tremendously, and enhanced accuracy. One large European bank used digitisation to improve approval times for SME loans from 20 days to about 10 minutes, according to McKinsey, which in turn increased win rates by 33% and margins by more than 50%.

More banks offer easier access to unsecured finance for term loan overdrafts, often facilitated by real time connectivity to credit bureaus or simple financial upload from any accounting package. A bank in Australia could lift its contribution to new small business lending from 21% to 37% within 12 months.

In markets such as Singapore, banks offer straight through account opening for SMES, and verification is completed through the phone or video conferencing. With full documentation, customers can get their accounts within the same day.

NAB reduced account opening time for a simple SME account, including KYC, from 14 days in 2017 to four days in 2018. Currently out of the 16% of accounts opened digitally, 80% of simple business transaction account applicants are being onboarded in less than 30 minutes via its new digital platform. Moreover, 92% of applicants are on-boarded on their first attempt with no rework required.

Front-line staff use digital devices to cross-sell and support SME customers far better. iSmart tablets at RHB Bank in Malaysia, for example, allow relationship managers to receive cross-sell lists automatically and enable them to assess SMEs’ needs, do peer benchmarking, use their financials to provide a health check, and offer product simulations.

Digitisation also allows SMEs to apply for loans and trade facilities or other services faster and more efficiently. The Mettle app from RBS Bank (UK) provides daily lists of overdue invoices and bills to pay, for example, while also allowing SME staff to match payments to outstanding invoices and prompt customers with tailored payment reminders from their mobile phone. DBS Bank’s digitisation reduced the number of fields in loan applications by 76%.

Partnerships

Banks have augmented their SME banking strategies by partnering with established service providers as well as fintechs to deliver services beyond banking through a business ecosystem. Key initiatives include the use of AI, non-financial services with freemiums, new ways of credit scoring, sub-segmentation, targeting for mobility and cashflow, payments and product bundling, and cross-selling more products.

In Malaysia, for example, Hong Leong Bank partnered with Biztory, an e-accounting and invoicing software solution, and Kakitangan, an HR platform, as well as SimpleTax, an online tax advisory tool, and Digital Advert, which supports outdoor digital advertising, to provide a full suite of services for SMEs. “The right functional tools will help them to be more agile and efficient,” said CEO Domenic Fuda.

In Australia, Westpac, and NAB are heavily invested via their capital venture funds into a series of fintech companies such as Valiant, a business loan market place that matches SMEs to the best lender or Slyp, which enables merchants to instantly send customers a smart digital receipt directly to the mobile banking app. The partnership is developing a range of smart receipt engagement modules that helps customers, merchants and banks to interact more meaningfully, including intuitive ratings, offers and seamless loyalty enrolment.

Analytics driven business

Banks are increasingly using advanced data analytics and digital technologies to develop personalisation and individualised experiences for the SME segment of one.

A bank in Thailand leveraged on the customer footprint to offer pre-approved credit lines upfront to selective customership. By looking at the sales growth, buyer supplier data and the income its recommendation engine increased conversion rates from 10% to 40%, while it equally could reduce the frontend fee to clients.

The San Francisco Federal Reserve Board (Fed) in the US said emerging financial technology expands SME access to credit in Asia by using alternative data to enhance credit analysis of SMEs previously disadvantaged by limited credit history and inefficient processes. Lenders may analyse an SME’s online sales and payments activity to assess their creditworthiness without a credit score, for instance, or use utilities and telco data to confirm on-time bill payments, and corroborate loan applications through geo-location data from telcos.

Value-Add Services

Banks are going beyond traditional banking to wrap together a wider range of services that help SMEs manage their administrative burden and grow their businesses in the area of cash management, productivity, market information and access. A sub-trend is pointing towards the merger of banking with accounting software.

CBA introduced a subscription-based management tool by combining accounting, payroll and banking, and operational functions, including HR, inventory and manufacturing. It is based on an an end-to-end, integrated, cloud-based business management platform which combines business management capabilities with online banking and payments, and integrates into other 3rd party software. Fees range from $49 to $190 per user per month with a one-off set up cost.

Bank of America in the US launched a free cash flow and cash management app called ‘Business Advantage 360’ to enhance its position in the small business segment. The digital dashboard, available on mobile and internet shows a streamlined view of key transactions, major expenses, credits and debits, includes automatic cash flow projections based on scheduled transactions. Business owners can set cash flow thresholds and manually adjust cash flow projections to account for additional data, such as new sales. It also offers the ability to connect with experienced small business bankers for guidance in just one click. Future capabilities of the tool are expected to deepen the cash flow insights, provide general market research and analysis, and enable clients to manage items such as payroll and human resources, payments and invoices, merchant services, tax accounting, goal-setting and forecasting.

Value added services often go beyond management tools. ING Bank ?l?ski in Poland, for example, launched Placeme, which supports entrepreneurs in finding the best place for their business. The app helps SMEs to find and assess locations with the best business potential, optimise sales and marketing, identify premises for a new business, and obtain information about competitors and consumer habits.

In Southeast Asia, UOB Bank’s FDI Advisory Unit offers a one-stop service for foreign companies looking to set up regional operations, with insights on the nuances of local markets, market-entry support, and support for partnering with government agencies or business associations.

Case Studies

OCBC Bank, Singapore

OCBC partnered with a fintech from New Zealand to go ‘beyond banking’, building an ecosystem to support SMEs. It puts the services into an open platform, since SMEs have low budgets, and gives them bite-size tools to operate better. The platform works with more than forty apps, including Xero, QuickBooks, Mailchimp and Shopify, to provide HR, accounting, marketing, ecommerce, productivity enhancement, inventory management services and more. “We give it to them, and they get a discount,” said OCBC Bank executive vice president Tan Chor Sen.

The other big play is the bank’s investment in e-KYC. “In banking, the heart is e-KYC,” Tan said. Banks need to do KYC for onboarding as well as lending and transactions. OCBC can now onboard brand-new customers in as little as eight minutes.

OCBC is also seeking to eliminate SMEs’ two key pain points, not having information at their fingertips and being time-short, with a widget-enabled dashboard powered by vendors such as Vend, QuickBooks, Xero, Shopify and Wave. Customisable drag-and-drop icons show the financial health of their business. information such as stock management, who’s working, balances and daily sales. “It’s like an iTunes store, an app marketplace,” Tan explained. “The marketplace curates apps based on your industry.”

RHB Bank, Malaysia

On its digital journey, said Jeffrey Ng, RHB head of group business and transaction banking, RHB has been building an ecosystem for SMEs and works with cloud-based providers to deliver accounting, POS and payroll services. “Partnerships are the way to go,” Ng said. “The connected ecosystem. We have workshops together, cross-sell, and give a complete solution to an SME.” APIs between the Bank and its partners allow a two-way feed to improve SMEs’ efficiency.

To make banking easier, RHB has put together a customer-initiated solution whereby SMEs can apply for financing through an online portal in 10 minutes, with just a bank statement and an identity card, and receive in-principle approval in two days.

Ng said a new API with a third-party provider will fundamentally change how RHB gives financing to SMEs. “We have come up with solutions that meet particular needs. We can link to anybody in the market. Going forward, data will open the door for higher wallet sizing and lending.”

PayPal Europe

While PayPal is best known for ecommerce and POS payments, said Norah Coelho, senior director for business finance in Europe, it saw an opportunity to leverage its data and relationships with small businesses to provide working capital financing.

Customers that have had an active account with PayPal for at least three months can apply for working capital loans 24/7, without having to go to a bank branch or furnish a stack of documentation. PayPal uses a proprietary underwriting model and data on factors including the frequency, volume, regularity, and concentration of sales as well as shipments and inventory to make a decision on a loan, which can range from $ 11,500 to 192,000 (£9,000 to £150,000 in the UK. In Mexico, it has partnered with Konfio to use alternative data for credit assessments. Merchants then pay the loan back out of their sales. Coelho said merchants tell her that, “the ability to get capital quickly, to have funds in the account, is a tremendous value.”

In addition to loans and payments, Coelho said PayPal works with partners to provide more services to merchants, including Intuit or Xero for accounting and Sage for invoicing. And going forward, Coelho said, PayPal is, “always looking to bring services outside lending, the core payments business, to enhance tools and bring more to customers.”

Staying Ahead requires Innovation

While fintechs may take some market share away in specific niches, the partnerships, analytics, and value-add that leading banks are developing can keep head of the game. Banks that fail to keep up could lose a significant share of their SME business.

.png)

.png)

.png)

.webp)