.png)

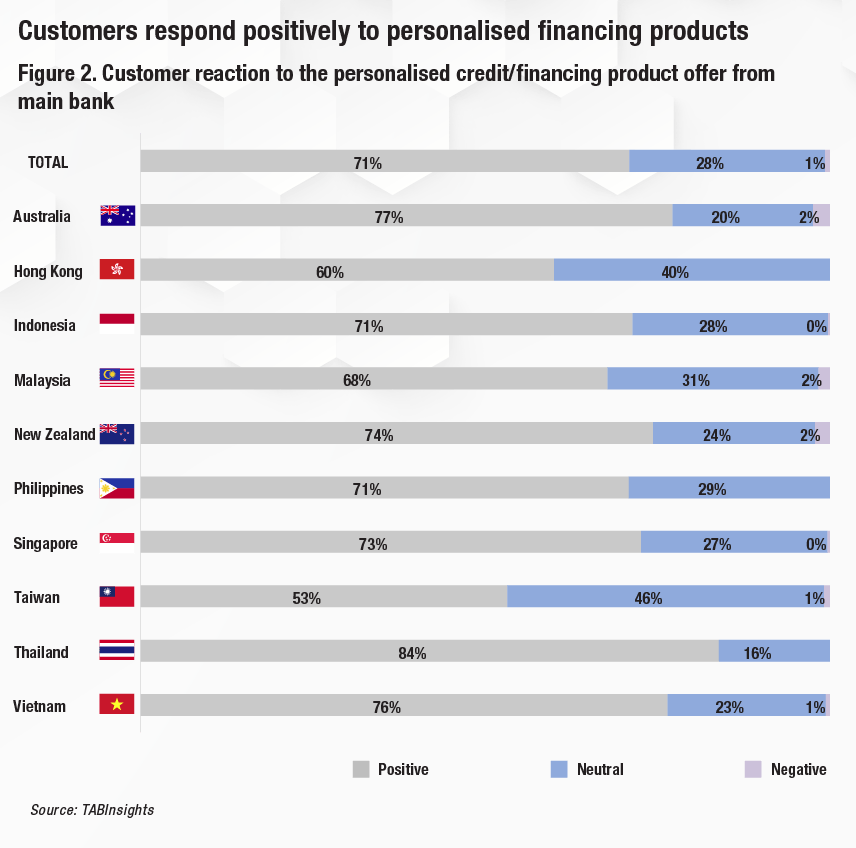

- 71% of consumers in APAC respond more positively to personalised products from banks, but providers in Australia and New Zealand are lagging behind

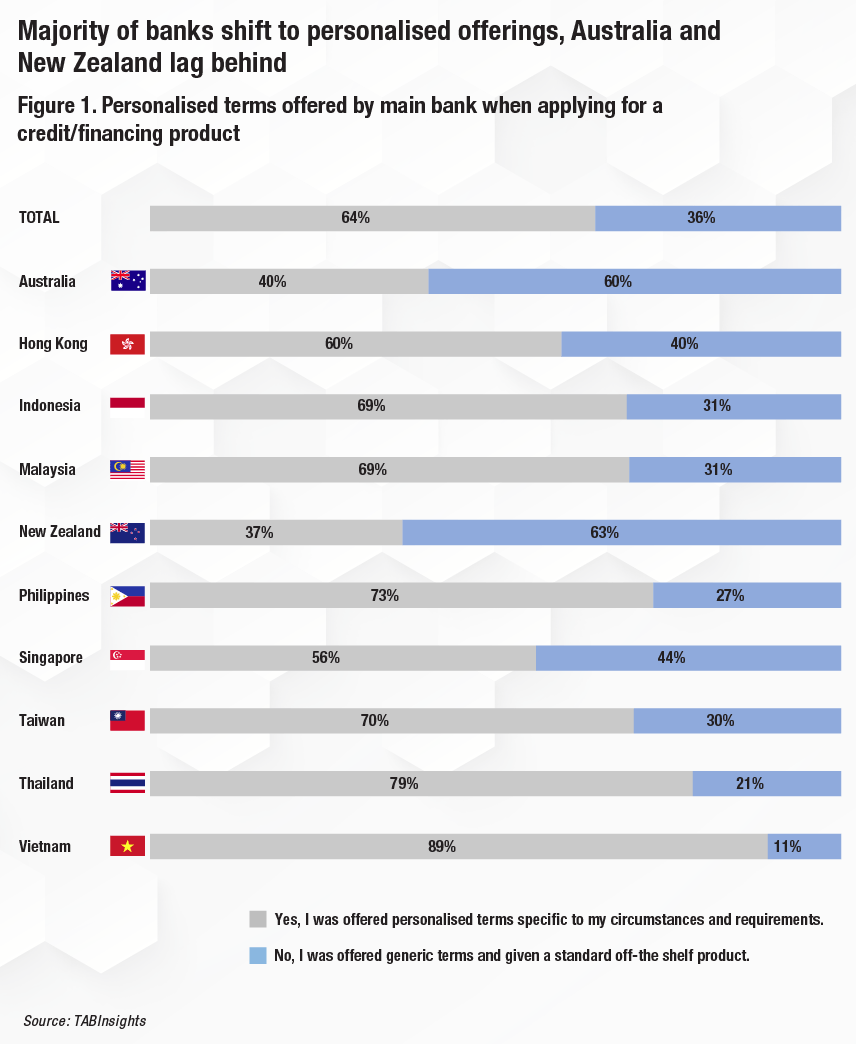

- 64% of consumers in APAC have received personalised products from banks, albeit lesser proportions in more developed markets such as Australia, New Zealand and Singapore

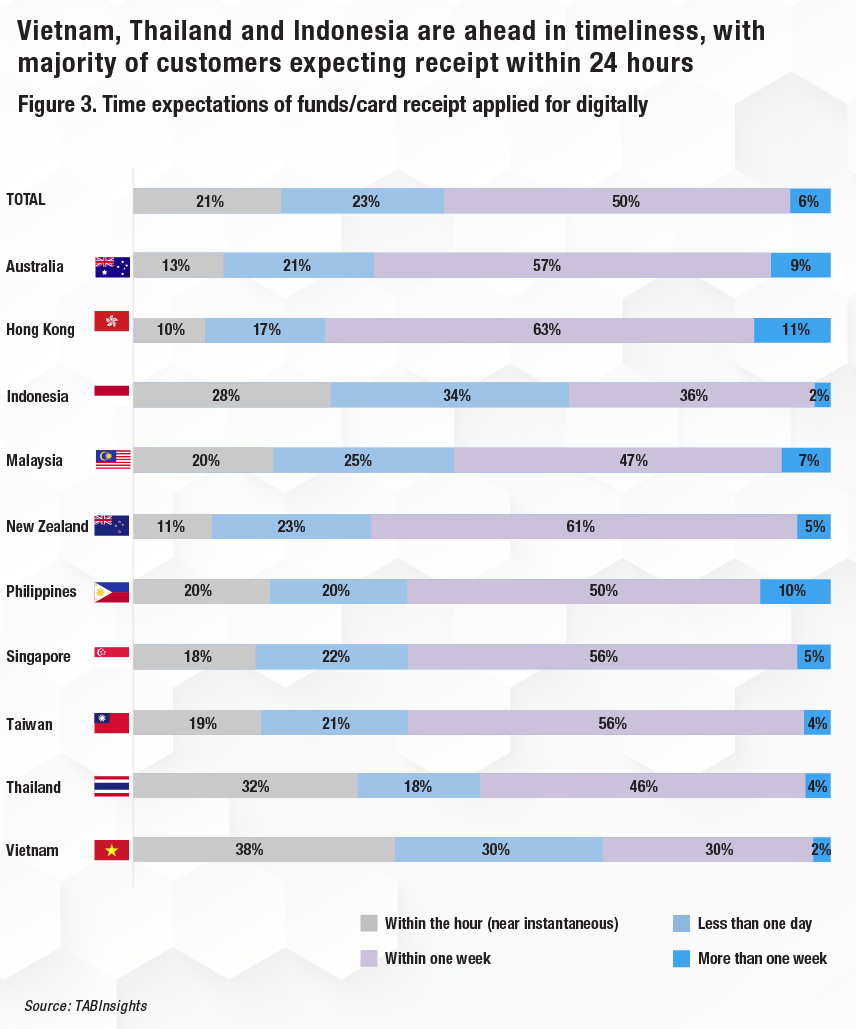

- 44% of consumers in APAC expects same day or faster funds transfers from banks, with expectation higher in emerging markets such as Vietnam, Thailand and Indonesia

In December 2020, analytics software company FICO commissioned TABInsights, the research arm of The Asian Banker, to conduct a survey across 5,000 digital banking customer respondents in 10 key Asia Pacific (APAC) markets, namely Australia, Hong Kong, Indonesia, Malaysia, New Zealand, the Philippines, Singapore, Taiwan, Thailand, and Vietnam. The survey provided insights on banking consumer preferences, interactions, and engagements. The study also highlighted the importance of deeper personalisation in consumer finance products as the key driver for customer satisfaction and a smoother digital banking experience.

For banks in the region, the ability to effectively offer customised products and services is an important component of ensuring competitive advantage in a landscape dominated by big tech companies that have redefined customer experiences via tailored interactions. Banks have responded to the challenge as the application of big data and analytics has provided a better understanding of customer needs, but meaningful experiences remain uneven and inconsistent, leaving some pain points unaddressed.

Likewise, enabling successful customer journeys has necessitated a departure from maintaining a sales-centric approach to one that is focused on predicting customer needs, developing trust, and creating value. Rolling out a true “segment of one” marketing strategy in today’s fast-evolving banking landscape that has undergone sustained disruption will require delivering unique and impactful experiences. Aashish Sharma, FICO’s senior director of decision management solutions in APAC, said, “The divide between companies that can deliver a personalised experience and those that can’t, continue to grow every day”. He added, “Consumers want to be treated as valued customers and not just another number”.

More banks shift to personalised counter offers, encouraged by customers’ preference

Lenders are cognisant that to compete effectively in today’s retail financing environment, speed to market and pricing features may be insufficient and the greatest value-add is centred on products that are bespoke and tailor-made to meet the specific needs of the customer. For the most part, this thinking has permeated across institutions in APAC but a distinct disconnect remains in Australia and New Zealand where 60% and 63% of respondents respectively have indicated otherwise (see Figure 1).

Customers are looking for further control over their personal financial management. Having financing products structured to meet their specific needs will help facilitate that process through reduced costs and greater opportunities to realise financing objectives. The response by surveyed customers for personalised offers has been comprehensively positive (see Figure 2), while standard financing products have been predictably less well-received.

Aashish asserted, “For banks we know there are significant opportunities. Our survey of APAC consumers showed there is growing dissatisfaction and a lack of interest in generic credit offers with around eight in ten people having a negative or neutral view. In contrast, personalised approaches get cut-through with around seven in ten people reacting positively. So, it is clear that cross-sell and upsell opportunities exist for those lenders keen to harness decision management technologies”.

The cohort of respondents who have been extended customised solutions from their main bank have reacted positively. It shows the value in personalisation when compared with generic offerings. Banks’ failure in connecting with clients through unique and differentiated financing solutions inhibits the possibility of a superior customer experience, limits the development of long-term customer relationships and reduces commercial potential of further cross-sell and upsell opportunities.

Banks are competing with fast-acting fintech alternatives

The rapid availability of new financing for customers is essential to developing and consolidating main bank relationships on a long-term basis. Given the real-time transactional experiences on other platforms, customers have now began to expect similar engagement from their principal lender. While a one-week waiting period is generally acceptable for most borrowers, there is a desire for most customers to have access to loaned funds even sooner, whether it be within a day or even an hour, which fits within the evolving personalisation paradigm (see Figure 3).

“We have seen in the survey that customers feel most comfortable with their main bank, especially during times of hardship. This trusted partner relationship is a significant factor, but one that will come under pressure as consumers start trying and perhaps liking the newcomers,” Aashish pointed out, referring to the emergence of fintech alternatives as they improve on the lending and financing experience of customers.

Gaps remain in existing bank personalisation strategies

Capturing greater customer share of wallet will require re-imagining the entire digital lending process, particularly within the context of personalisation. Surveyed respondents remain relatively positive in terms of the ease of use concerning the various application channels for seeking new financing and with the consistency of product information delivery across different touchpoints (see Figure 4). A seamless experience being provided on an end-to-end basis was still questionable for some. More importantly, enticing incentives for new product uptake were missing, thereby limiting the effectiveness of both customer acquisition and engagement strategies.

Aashish asserted, “One area that is critical to consider when looking to improve the customer experience is all elements of the customer journey, especially those less travelled. It is important to plan for the ‘unhappy paths’ that might get thrown up for a customer. We see a lot of this in banking, where a customer will abandon an application because they have been asked to complete a task outside of the channel they are using. Banks risk losing a significant amount of business unless they can streamline these experiences and use technology to help reduce friction for the customer”.

Digital banking is a key enabler of customer optionality

Leadership in digital banking will require adapting to evolving customer needs proactively while addressing customer pain points and ensuring a frictionless customer experience. The case for new end user personalised experiences has been made quite categorically. Digital product offerings and service capabilities will be re-engineered to enable customers to have greater control over how they choose to engage with a bank while accessing customised solutions. Technology is reshaping how consumers access financial services, and greater communication on how it can be leveraged to enable meaningful experiences is needed.

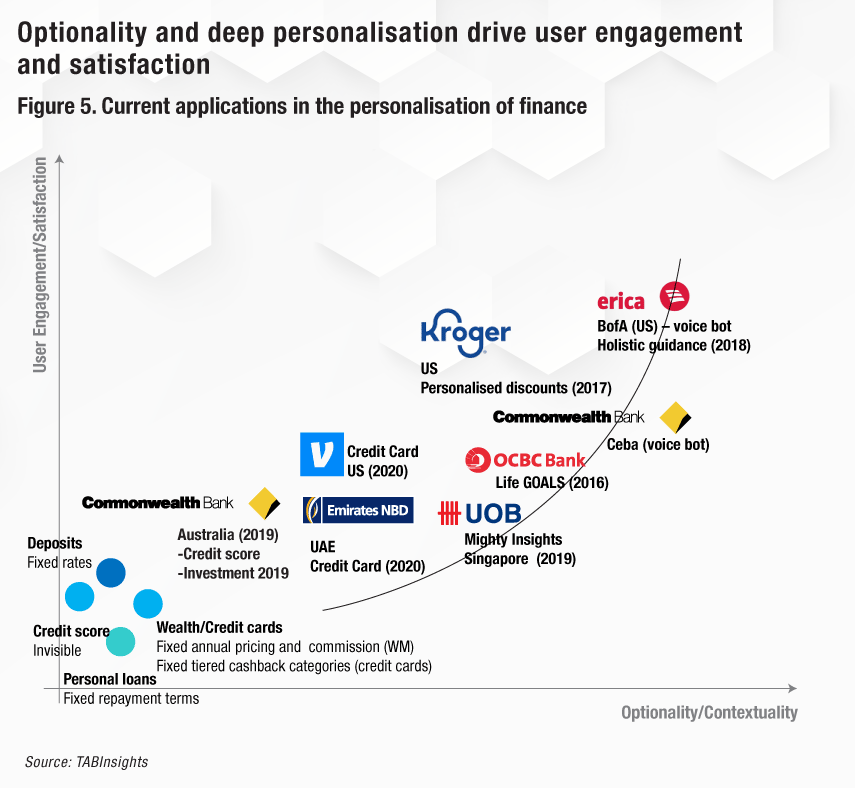

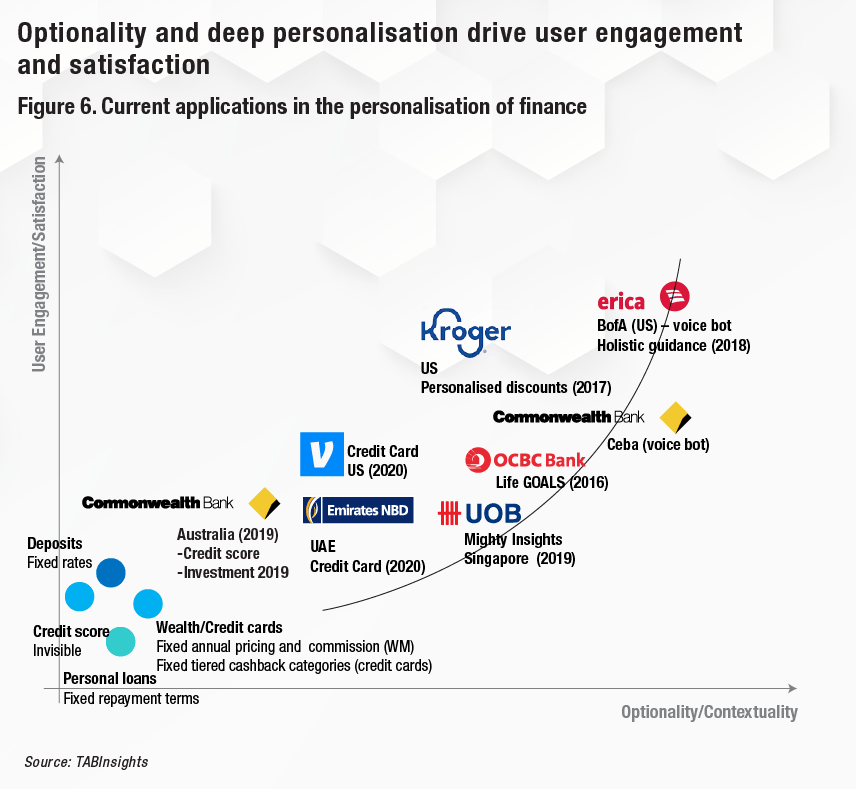

As banks in the region have focused on digitisation and automation of core lending and payment processes for better convenience, there is little emerging that points to embedded optionality with regard to services and products compared with what is being observed globally (see Figure 5).

For the personalised services, a restructuring of the value chain is often needed potentially through open banking partnerships for instance. Whether it is Bank of America’s Erica, a standard-setting financial chatbot powered by conversational AI that has made it easier for customers to navigate functions offered through the bank’s app, or Commonwealth Bank of Australia’s CommSec Pocket app that has simplified investment decision-making by providing seven different investment themes to choose from, the thrust has been allowing customers to take ownership and control.

This approach is further exemplified by the Emirates NBD Visa Flexi Credit Card that was launched in October 2020 with a view of addressing the constantly evolving needs of customers by enabling them to directly select benefits. For cardholders, this product can be adapted to their unique lifestyle as customers are in a position to draw from a broad spectrum of spend categories including travel, entertainment, lifestyle, and sports. New benefits can be added to the catalogue by using Visa's application programming interfaces to integrate with benefit partners, while ensuring a complete digital journey for the customer.

Aashish cautioned, “For traditional players to succeed, they will need to compete with their own digital strategies to ensure they maintain their incumbent advantages over the challengers such as their customer base and data. Some banks have bought fintechs, others have created new divisions, while some look to rebuild some of their offerings from the ground up. Capturing a greater market share as well as share of wallet will depend on how successful these strategies are and how quickly banks can use big data, machine learning and decision management technologies to keep their customers and win over new ones”.

Achieving personalisation at scale within personal financing will not only require a thorough understanding of customer needs but a proactive engagement with customers with a view towards maintaining long-term main bank relationships built on impactful customer engagements. Technology will play a central role in delivering these unique experiences across all channels with a single customer view. Fundamentally, digital banks will be embedded to support the lifestyle needs of customers while providing the perfect blend of advice, options, and convenient service.

.png)

.webp)