- Traditional payment platforms saddled by low-margins and competitive pressures

- Alternative payment integration providers seeking market expansion look to replace Wirecard in Asia-Pacific

- PayPal and CUP stand to benefit from Wirecard’s demise provided interoperability issues are addressed and trust is restored

German payment processing platform Wirecard has been exposed for its financial reporting malpractices as the firm recently admitted to the loss of $2 billion worth of funds. It led to the resignation and arrest of its CEO Marcus Braun and the company filing for insolvency. The company’s profitability has been closely scrutinised given the low margin nature of the payments business especially for payment processing companies. Although payment is one of the most dynamic industries in financial services, competition has become very fierce and new technologies have led to the commoditisation of the business.

Implications of the low-margin payment processing business

With the introduction of cryptocurrencies and entry of not just fintechs but big techs such as Amazon, Apple, Google and Facebook, boundaries are being pushed when it comes to efficiency and price. Because of the crowded payments arena, processing platforms have seen increased pressures on fees and margins as they fight for market share and processing volume.

Michael Bellacosa, global head of payments and transaction services at BNY Mellon opined, “there are two key factors that have resulted in a steady downward push on fees and margins over the last several years. The first is the influence of new competitors, particularly as regulators have been more open to adding participants in the payment market to help drive innovation and reduce costs. The second is that there has been significantly more transparency built into cross border payment services, which has allowed users to better assess a total cost comparison”.

Dhiraj Bajaj, head of Asia Pacific financial institution sales at Bank of America echoed similar sentiments, commenting that “increased competition in the space has led to pressure on payment margins (fees and FX) and companies are spoilt for choice as several players compete for market share”.

To survive and achieve profitability, payment processing platforms must offer other valuable services and generate mega-scale. In 2019, a number of large payment consolidations occurred with Fidelity National Information Services (FIS) acquiring WorldPay, Global Payments completing its merger with TYSYS and Fiserv buying First Data.

Traditional incumbents are responding, Bajaj remarked that “over the last decade, banks have made significant investments in new technology and the emergence of fintech companies in the domestic payments and cross-border remittances space have led to improvement in speed, transparency and digitisation of payments”.

Wirecard’s takeover of “on-us” payments

Founded in Munich in 1999, Wirecard began as a payment processing platform helping internet sites collect credit-card payments from customers. In 2002 the company was requalified to service payment transactions for various web-based gambling portals and adult entertainment websites. CEO Markus Brown’s vision was to provide the technology for facilitating cashless payments benefiting both companies and consumers alike. Wirecard embarked on an aggressive expansion path in the e-payments landscape that started initially with the launch of a Visa and Mastercard credit card division in 2005 followed by its strategic partnerships with American Express, Apple Pay, Alipay, Discover, China UnionPay, JCB and WeChat Pay.

The 2007 establishment of its Asian subsidiary in Singapore, which would later play an important role in increasing the group’s revenue, was an important milestone in the company’s development as strategic investments in Asian mobile payments that ensued allowed Wirecard to endure the 2008-09 global financial crisis.

Wirecard’s business model encompassed cashless payments across a vast network of credit card companies, retailers and banks. Given that Wirecard was able to process payments and issue credit cards resulted in increasing complexity in the flow of payments from customers, companies and banks. On pricing, Wirecard differentiated itself from competitors by claiming to offer greater transparency on pricing with reduced and consistent fees charged to merchants.

The successful rise of a regional processing company

As a survivor of the dotcom bubble burst of 2000, Wirecard had a focused strategy of an enabler of secure online payments. The global growth of e-commerce transactions naturally resulted in an increased demand and opportunity for payment processing technologies. Following its 2006 acquisition of XCOM, Wirecard continued its evolution as a full-service payment operation that disrupted the emerging e-payments landscape by focusing on online and contactless payments as well as fraud prevention systems, while also facilitating online businesses with the requisite software and systems to remain plugged in to the wider global financial system.

Notes:

1. Wirecard’s annual transaction volumes from 2010 to 2019 were reported figures, as of 22 June 2020 and subject to revision

2. The investment from SoftBank is now being reconsidered

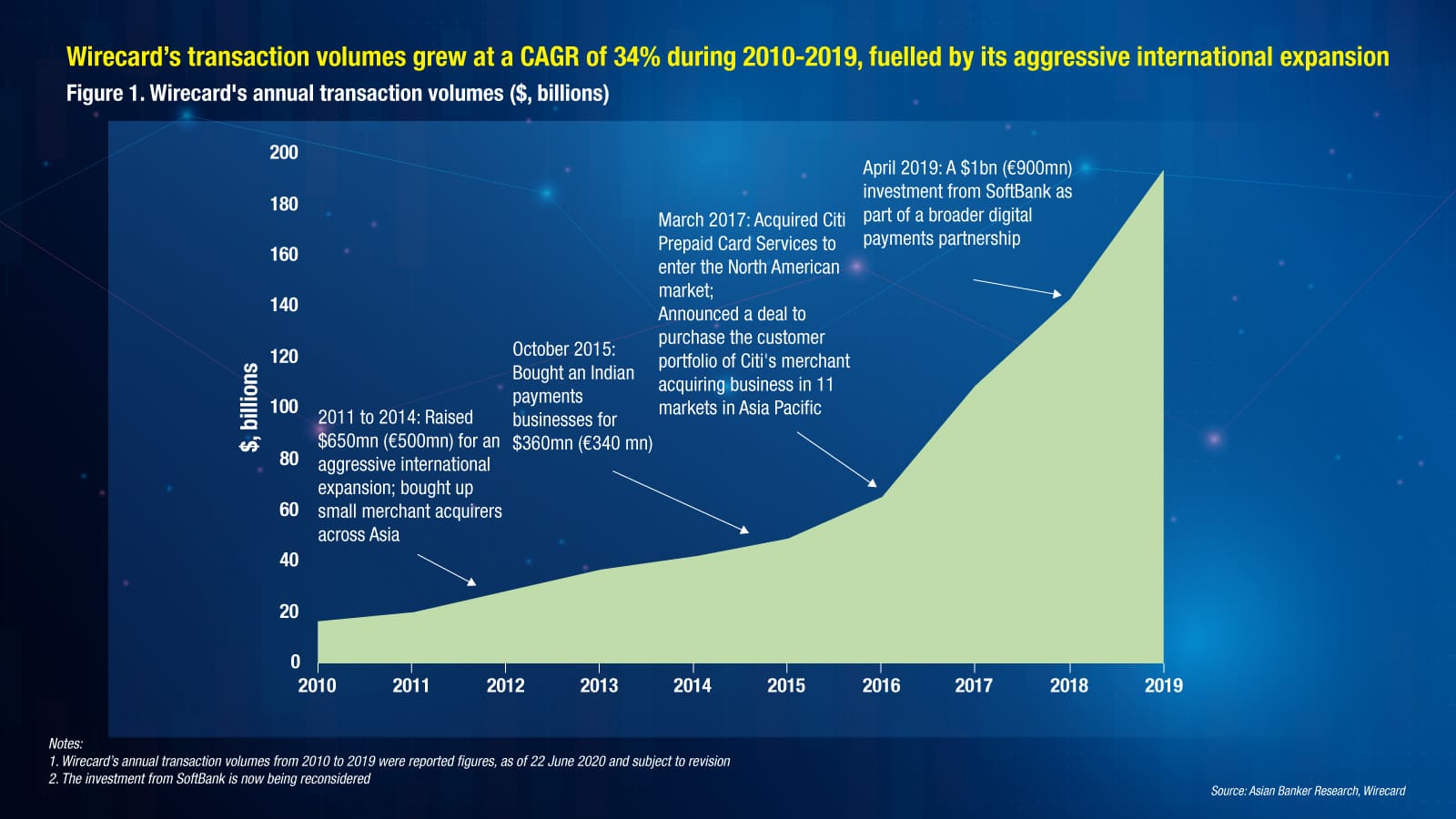

From 2011 to 2014, Wirecard introduced wireless payment solutions that helped the company source $562 million in new funding from shareholders and kickstarted further international expansion. It strategically acquired smaller payment companies throughout Asia while opening new offices in Australia, New Zealand, South Africa and Turkey. In 2015, Wirecard entered the Indian market while it also separately launched Boon – a smartphone specific payment software. By 2017, Wirecard had procured Citigroup's prepaid bank card division that operated in 11 countries. Importantly, it gave Wirecard a foot in the door to the North American markets. This was followed by the 2019 rollout of digital wallet boon Planet which enabled Wirecard to stay ahead of its competitors.

Within 20 years, Wirecard had positioned itself on every continent, serving more than 313,000 customers across 26 locations. It last reported an annual turnover of $3.1 billion. It had also overtaken Deutsche Bank to emerge as one of the most valuable financial services firms on the German DAX index. Interestingly, while its balance sheet swelled with intangible assets such as goodwill and customer relationships during this period of rapid expansion, investors still believed and invested in the company that was transforming the payments landscape and generating healthy returns.

By 2018, Wirecard had categorically positioned itself as a financial technology innovator and white label code developer that provided the opportunity for companies to build their own online payment systems. Unfortunately, reports emerged in 2019 that half of its business is actually outsourced and payment processing was actually being conducted by external partners with Wirecard receiving commissions that contributed to the allegations of fraud and misrepresentation.

Alternate payment integration providers see opportunity to grab Wirecard’s market share in Asia

While it is too early to make the call, and Wirecard and its clients are navigating through the complexities and uncertainties of the liquidation proceedings, what is likely to happen is that more merchants will gravitate to dual payment integration providers, shedding reliance on a single one. Wirecard’s geographic expansion into Asia Pacific (APAC) has been driven by the third-party-acquirer (TPA) business model where Wirecard leverages its network of local partner processing companies (that hold banking licenses) to penetrate the region’s online payment market.

With Wirecard Group now filing an application for bankruptcy proceedings over impending insolvency and over-indebtedness there is a high level of uncertainty that customers and merchants with Wirecard accounts will face over their business transactions. The ongoing tussle may be further exacerbated should Visa and Mastercard take ‘actions’ on licenses that permit Wirecard to connect customers with the international payment networks operated by them. Naturally, this leads us to the question as to which alternative payment service providers (PSPs) in the region are capable of taking over the payment processing business of customers that disengage with Wirecard.

While there is no one simple answer, payment/transaction volume size and scale of operations, available market share of revenues by region, fees and processing rates charged, diversified product portfolios are some criteria’s that customers may consider for forging new integrations. As Bank of America’s Bajaj explained “many payment aggregators and payment processing companies have historically competed on price reduction, expediting time to payment and a superior technology experience to gain market share. In the current scenario, the focus should be on creating value and charging fees/FX in line with market pricing equilibrium and focusing on increasing market penetration and the size of the overall market.”

Given the fall of Wirecard it is important to assess the possible beneficiaries that stand to gain by this displacement. The next section delves into potential winners in the payments processing space.

WorldPay and PayPal well-positioned to leverage their leadership position in payments

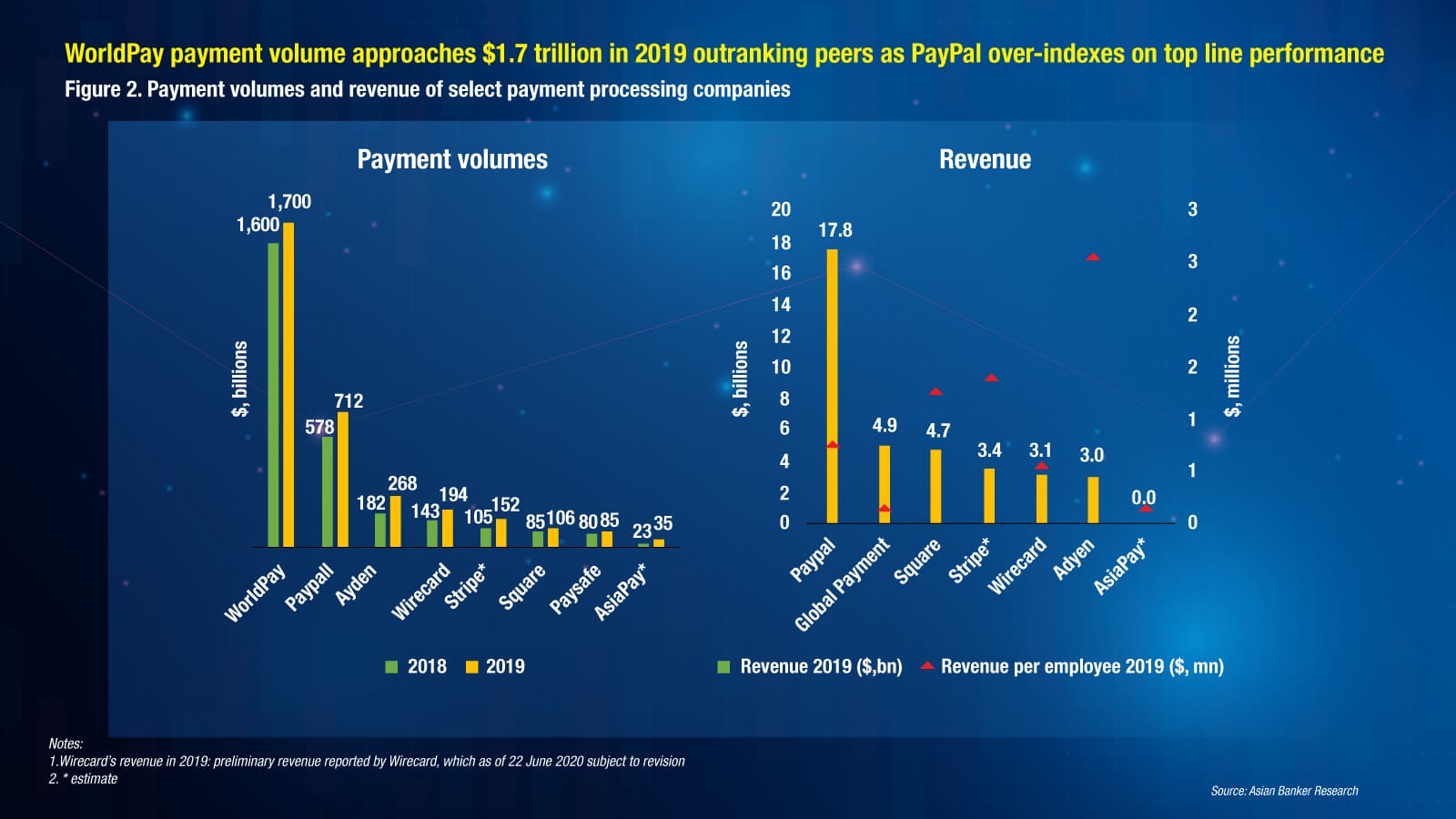

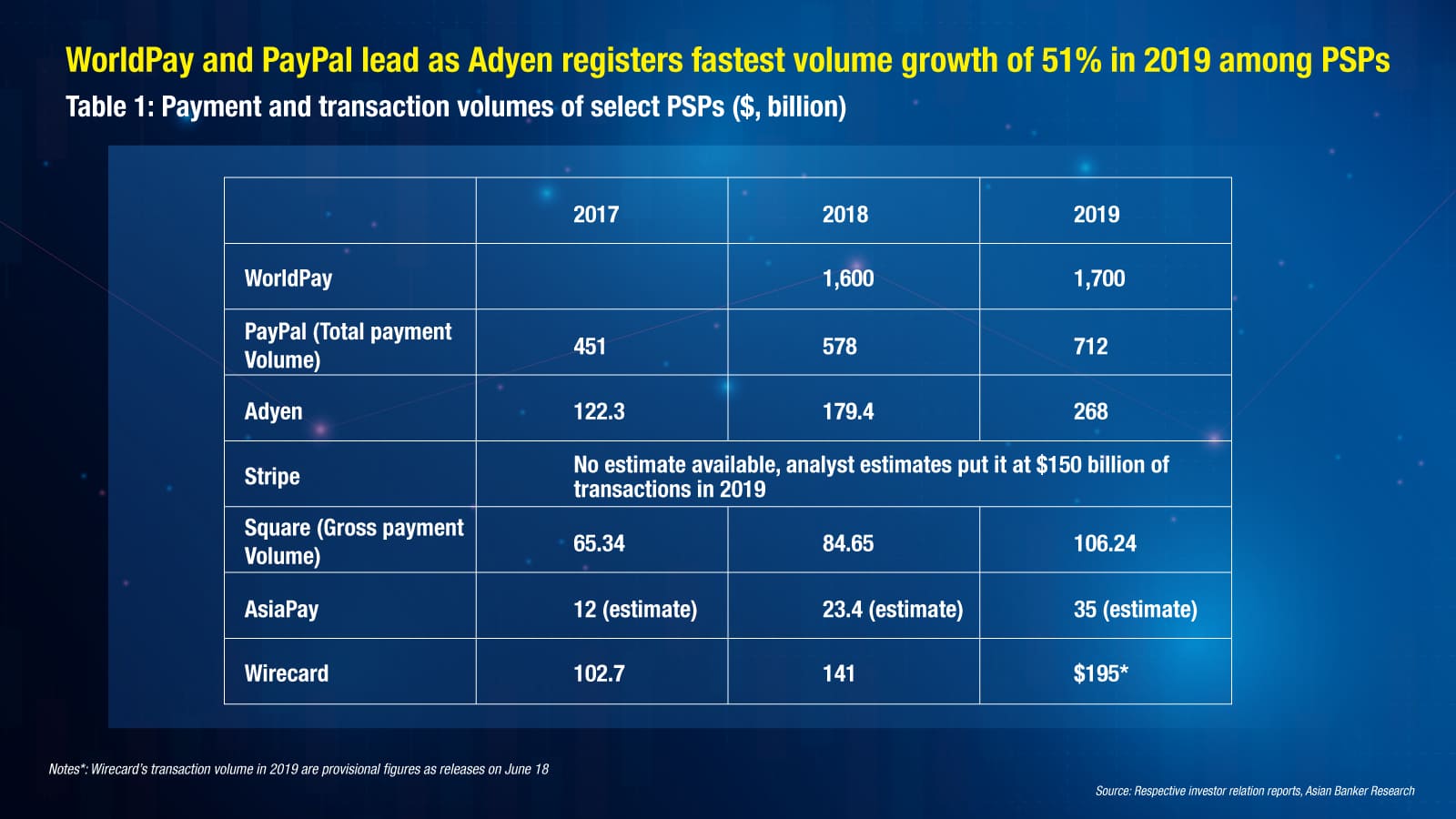

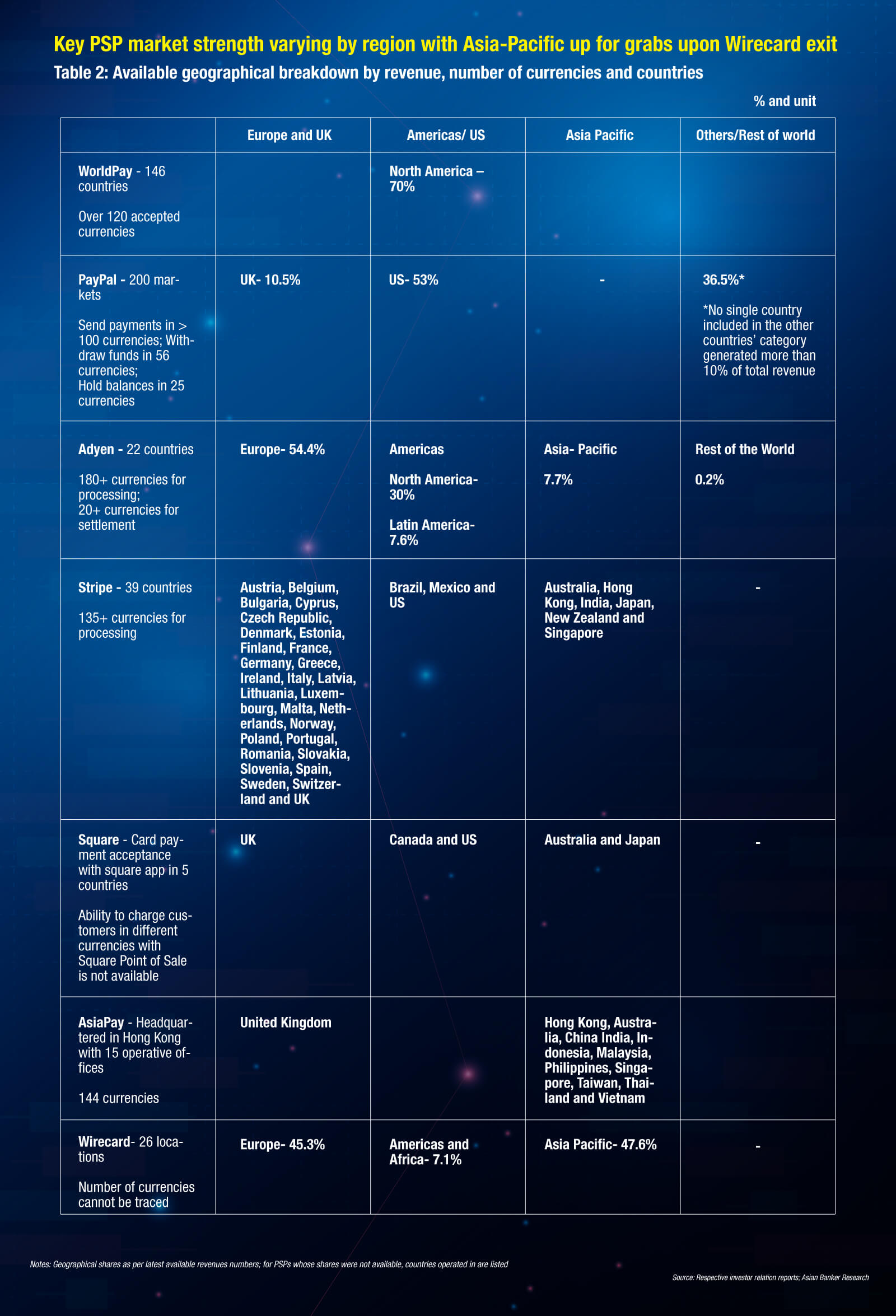

There are a number of strong direct competitors that could fill the vacuum left by Wirecard including WorldPay, PayPal, Adyen, Strip, Square and AsiaPay. From a payment volumes perspective, WorldPay comprehensively dominates as its deep engagement with key merchant accounts in North America generates recurring transaction flow. Likewise, PayPal’s scale and operational presence continues to drive its growth with total payment volumes expanding by 23% to $712 billion in 2019 (see Figure 2) while currently servicing over 305 million active customers (of which 24 million are merchant accounts) in 200 markets. This global setup gives PayPal the competitive advantage to integrate with more platforms in different markets enabling broader offerings that cover checkout, online invoicing and app payments.

Notes:

1.Wirecard’s revenue in 2019: preliminary revenue reported by Wirecard, which as of 22 June 2020 subject to revision

2. * estimate

Similarly, Adyen processed payment volumes of up to $268 billion (see Table 1) in 2019 driving its 51% growth through the onboarding of new verticals such as quick-service restaurants. Launch of Adyen card issuance further added to its volumes as it enabled clients to provide virtual and/or physical cards to their customers. Stripe also provides payment services for businesses in over 39 countries and stands out for its advanced API capabilities, with more than 3,200 core APIs while also deploying developer-centric online payment options allowing businesses to establish customised e-commerce processes.

Notes*: Wirecard’s transaction volume in 2019 are provisional figures as releases on June 18

Interestingly, Square’s gross payment volume totalled $106.2 billion, increasing by 25% year-over-year in 2019. Square offers relatively superior in-person point-of-sale (POS) related solutions and is regarded the go-to option for businesses that run more physical operations. As of November 2019, Square’s hardware products are available at over 24,000 retail stores, however Square outreach is very US and UK centric, and very limited in Australia and Japan, the only two countries it has presence in APAC.

While data to assess the depth of market coverage is limited, a breakdown of the latest available revenues by region (see Table 2), operational presence and currency service facilities could be useful. Having more foreign currency offerings may also ease burden of installing full payment operations in new geographies.

Notes: Geographical shares as per latest available revenues numbers; for PSPs whose shares were not available, countries operated in are listed

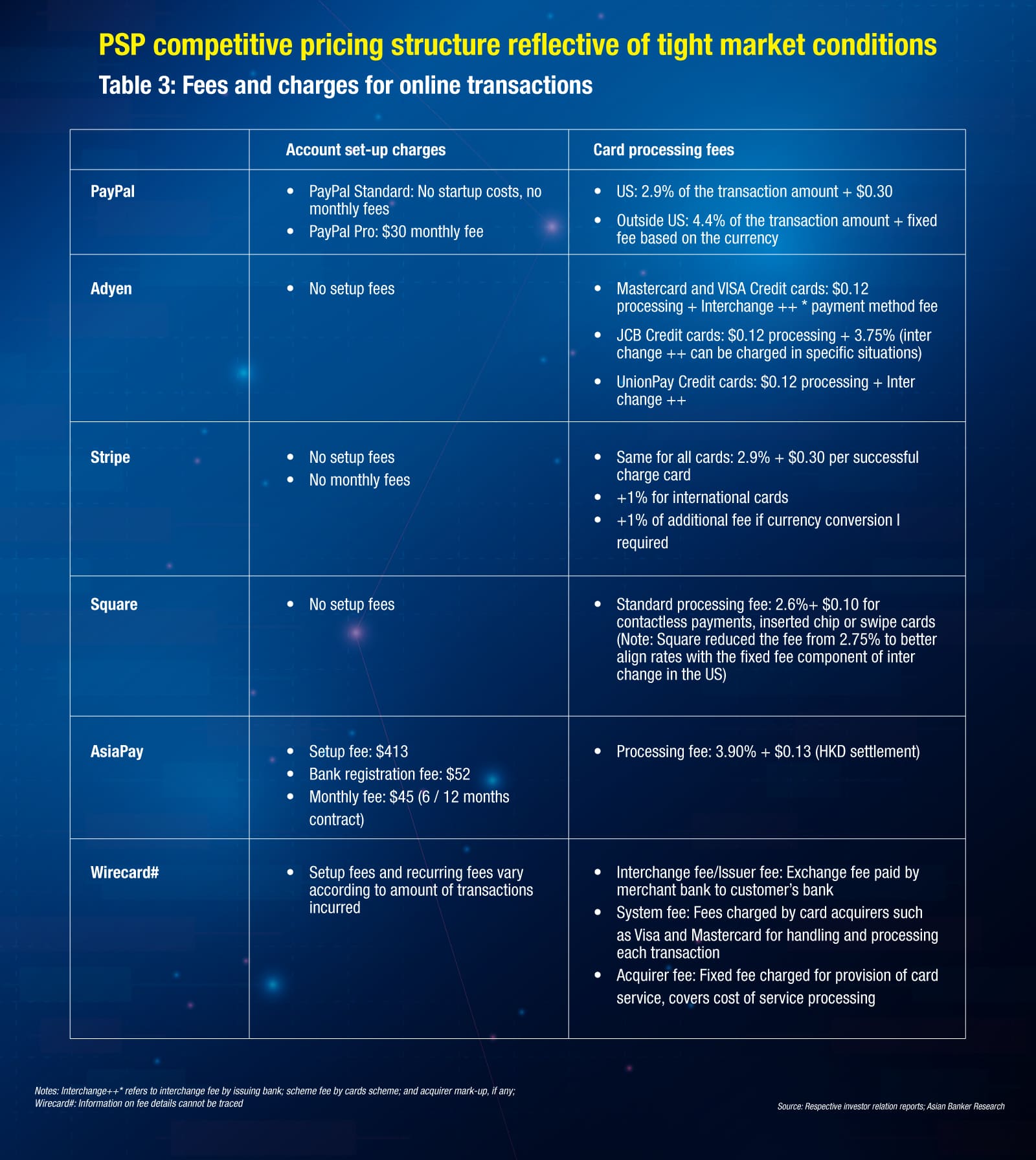

When it comes to fee comparison, it is never a simple exercise as there are various pricing models (see Table 3) that may depend not only on their own structure but jurisdictions that they operate in. For simplicity sake, we only list cost of processing for cards and account set-up charges.

Notes: Interchange++* refers to interchange fee by issuing bank; scheme fee by cards scheme; and acquirer mark-up, if any;

Wirecard#: Information on fee details cannot be traced

In comparing processing fees (see Table 3), it appears that none offer a ‘material’ significant advantage. Stripe and PayPal appear to be on par but PayPal charges higher international rates, but also brings to the table best possible integration with all with common website platforms. Square has lower processing charges however its limited scale of operations means it is far from being the best candidate in APAC. Adyen offers a rich omni-channel experience as it also integrates with WeChat Pay and AliPay in addition to all major cards. Notably, Adyen has found popularity amongst technology companies such as Uber, Spotify, eBay, Microsoft etc.

Opportunity for Chinese payment companies to go regional

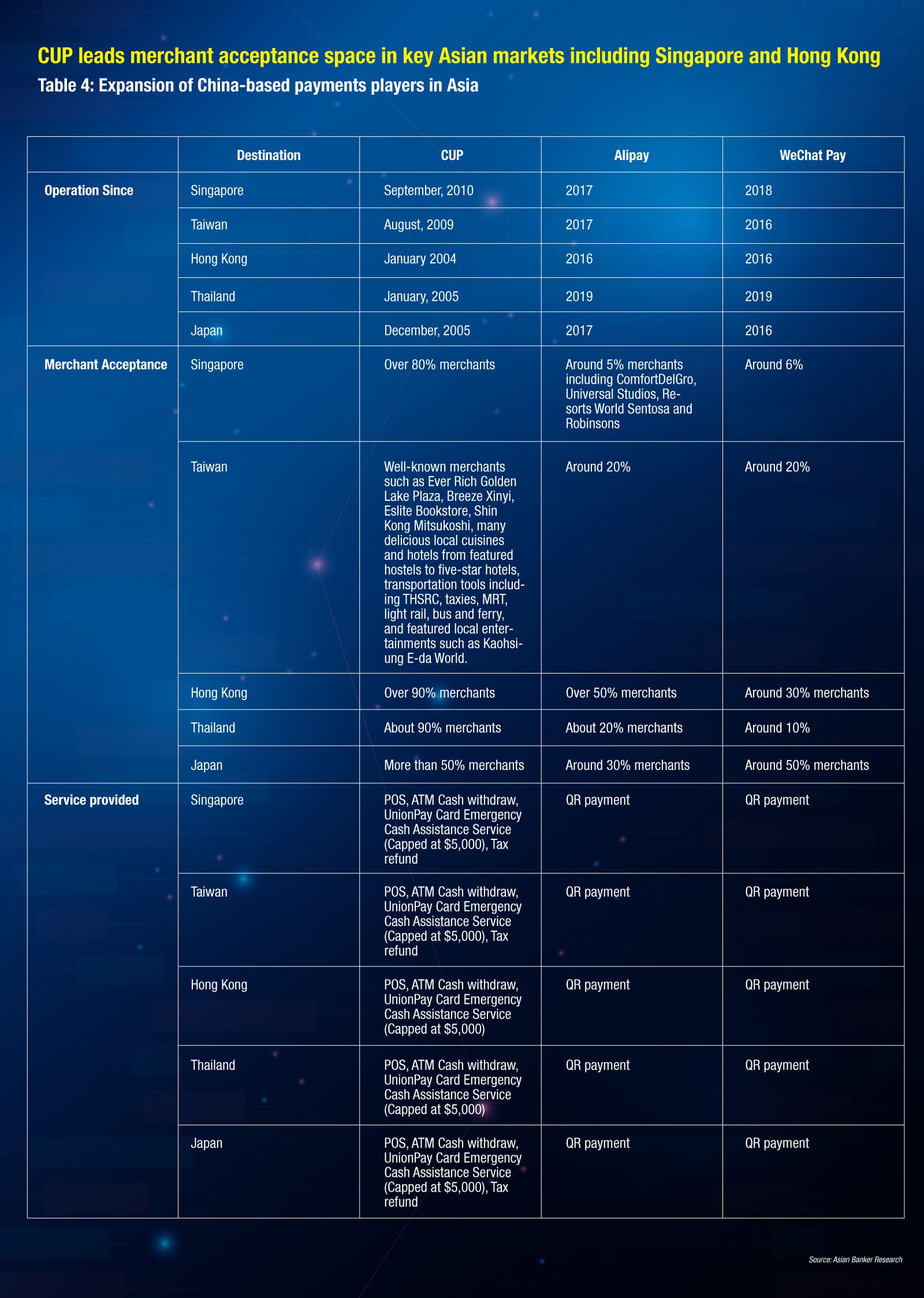

Chinese payment companies are monitoring Wirecard’s demise as the potential to move into the payment aggregation business within Asia, especially in select investment, trading and travel destination corridors. Chinese payment gateway companies and aggregators would be keen to support the cross-border flow of digital payment transactions. Although bank cards still dominate in the overseas payment markets, mobile based payments are now catching up. According to China’s State Administration of Foreign Exchange, 2018 registered as the first year in which more payments were made overseas by Chinese travelers using mobile payments than with cash. The trend continued in 2019 with mobile payments abroad doubling in the first half of 2019 compared to the corresponding period in 2018.

To facilitate the surging payment demand from Chinese visitors, Chinese payment companies and tech giants have stepped forward and the expansion is noticeable. Compared with Alipay and WeChat Pay, which are powered by their digital and QR code payment technology, China Union Pay (CUP) as one of the largest incumbents has successfully consolidated its payment infrastructure in key Asian markets. CUP has the largest acceptance ratio among merchants in top destinations for Chinese visitors. In markets like Singapore, Hong Kong and Thailand, CUP’s presence reaches up to 90% of local merchants. Kelvin Lee, managing director and head of Southeast Asia at Ripple, considers that “for merchants looking to offer preferred payment options in a diverse SEA region, this can quickly add up in complexity and fees. There is a need to break down silos in the payment process, and offer a universal payment solution that simplifies access for both consumers and businesses.”

Both Alipay and WeChat Pay were late comers in overseas payment services compared with CUP. The two companies have so far focused on getting merchants abroad to accept their digital payments facilitating Chinese travelers but neither firm has launched an international version of their respective apps for users based outside China. More importantly neither company operates as an aggregator within the dynamic Asian payment ecosystem but future forays in this space cannot be discounted whether through direct market acquisition of existing aggregators in the region or establishing its own standalone business. Since entering Japan in 2016, WeChat Pay had registered a six-fold increase in the number of transactions between June 2017 and 2018. Alipay had connected with 300,000 retailers, which marked a 500% increase in the same period. In Thailand, Alipay has signed a letter of intent with The Tourism Authority of Thailand (TAT) to facilitate the payment needs of over 10 million Chinese tourism every year. In the golden week of 2019 (1 October to 7 October), total transaction volume by Alipay in Thailand increased by 1.2 times compared with last year's total, with average spending per user increasing by 1.22 times. The two tech giants also provide value added services such as foreign exchange and tax refund in certain destinations.

What to expect next?

The demise of Wirecard has set in motion new opportunities for existing platforms in the payment ecosystem. Raymond Qu, CEO of Geoswift expects that “a number of fintech companies are expected to step in to fill the gaps.” However, the needs to maintain integrity will have now changed with Qu underscoring that “many institutional clients will place a stricter standard on due diligence to choose its payment service provider, and give more weight to credibility of the firm and the endorsement this firm may get from other credible clients.”

Qu further went to add that “payment companies are under much more scrutiny from internal processes as well, and make sure that they are fully compliant in the markets they operate. Such changes would provide an opportunity for our industry to grow healthily as a whole.”

It remains to be seen whether WorldPay, PayPal, Adyen, Stripe or CUP will be able to seize advantage of the vacuum left by Wirecard. As Ripple’s Lee remarked, “A major pain point that has been emerging due to rapid growth in the payments space for Southeast Asia is the lack of interoperable systems within each country, and across borders. This will be a key barrier to adoption of e-payments for consumers -- and there is a need for a simple and standardised payments experience so people find it easy to use for their everyday transactions.”

Lee further opined, “Southeast Asia is a hotbed of fintech activity, and the current climate has made it an opportune time for new entrants and financial technology companies to acquire customers. The Asian payments space is booming, and customers are starting to realise the benefits of instant, seamless and cost-effective payment solutions, with funds settled and transferred in real time -- challenging incumbent banks.”

Certainly, PSPs and payment aggregators will be looking to do just that. Whether some of the larger global payment players or local regional operators eventually succeed has yet to be determined as capturing any meaningful market share vacated by Wirecard will require institutions to first restore trust and credibility in the payment processing system.

.png)

.webp)