- Most global banks will support customers with both legacy and ISO 20022 payment during the transition phase

- Modern payment standards provide much richer data to enhance the scope of messaging, automation, payment processing and compliance screening

- Challenges around budget constraints, differences in market specifications, upgrade of legacy infrastructures and mandatory timelines persist

After an unforeseen and unintended delay caused by the COVID-19 pandemic, payment players are at last ready to start the global implementation of ISO 20022 - the new standard for payments processing, financial communication and electronic data interchange. The massive move towards digital payments catalysed by the pandemic has also made the adoption of the new standard now much more critical, timely and urgent than ever.

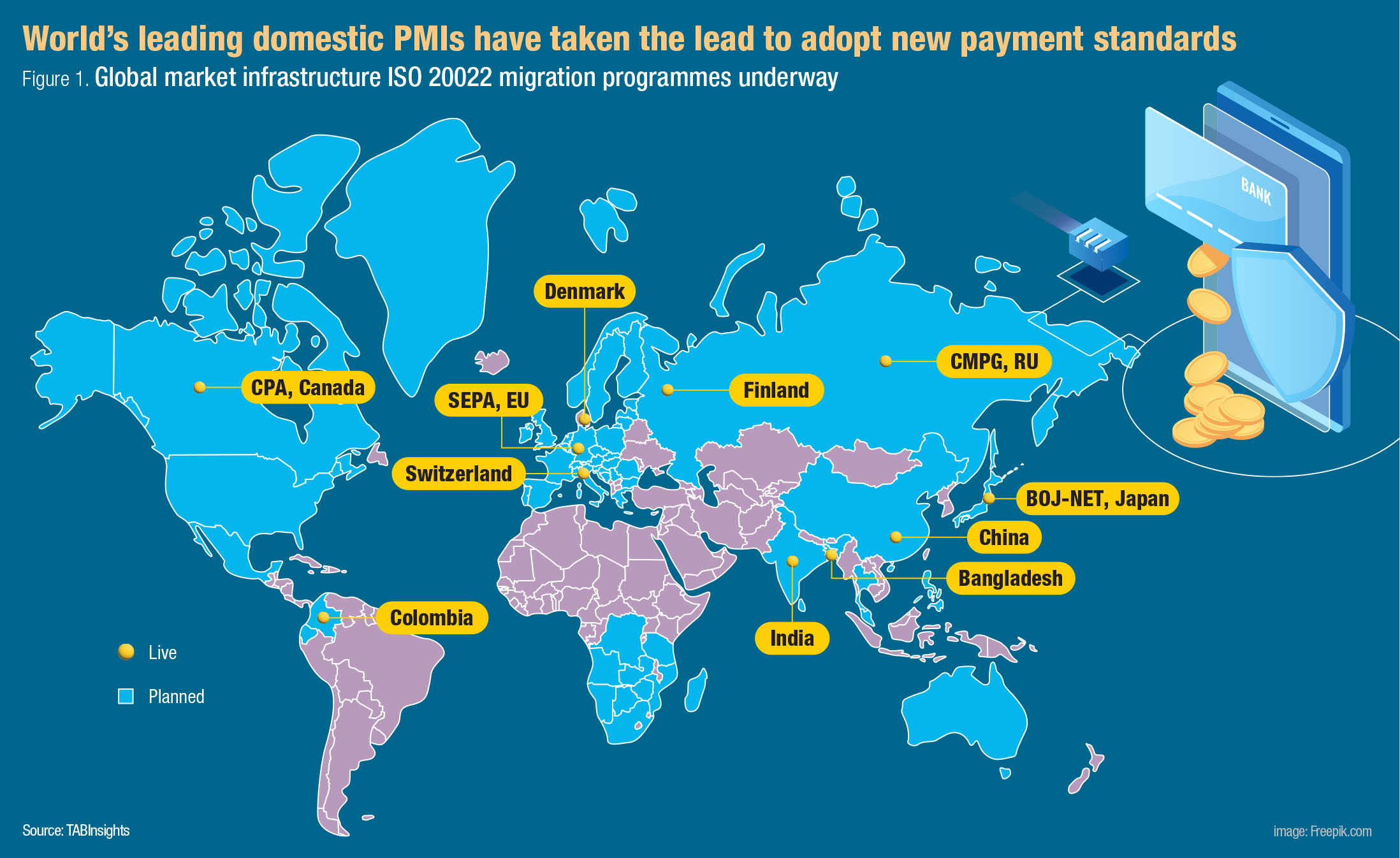

Some of the world’s major domestic payment market infrastructures (PMIs) have led the way to adopt ISO 20022 in payments processing, the onus now is on the financial services community to implement new and richer standards in cross-border payments.

SWIFT, the global payment messaging platform that dominates international settlement, plays an important role in the migration and adoption of the new standard for cross-border transactions. It started a three-step implementation process in 2020 that will culminate in November 2022, when it will go live across its networks. It will facilitate industry migration of cross-border payments and cash reporting as of end 2022. The migration will end by November 2025, when all financial institutions (FIs) will be required to send and receive ISO 20022 messages for cross-border payments.

XML ISO 20022 as opposed to SWIFT’s soon to be obsolete message type (MT) format, accommodates far more data components, resulting in richer information being transmitted while processing international payments. ISO 20022 also lays the foundation for greater interoperability, resulting in higher levels of straight-through processing (STP), auto-reconciliation and matching, streamlined compliance procedures and capability to deliver new value-added services.

All in all, as major global banks get ISO 20022 ready in 2022, early movers will be in a position to enhance cross-border payments experience and strengthen their overall customer and business proposition.

To support customers, both MT and MX formats will co-exist during the transition phase

As ISO 20022 standard gains impetus with the proliferation of instant payments, the adoption will drive changes to bank products and processes while they align systems to the new format. Most global banks will maintain both the legacy and new ISO 20022 compatible systems until the transition phase is over. “To minimise client impact during the migration phase, Bank of America will support both legacy and ISO payments and reporting format between November 2022 and November 2025”, said Dhiraj Bajaj, head of FI sales for Asia Pacific at Bank of America.

Dhiraj Bajaj

head of FI sales for Asia Pacific,

Bank of America

Girish Raju

Director of payment standards,

Standard Chartered

Co-existence of both formats also means that minimum system changes will be required by banks to plan for critical processes such as sanction screening, fraud detection and anti-money laundering (AML). “Given how some messages will enter receiving banks in multi-format (MT+MX), thus requiring parsing of MT messages and identification of possible data truncation from MX messages, minimum changes will be needed”, remarked Girish Raju, director of payment standards at Standard Chartered.

If adopted fully and used correctly, ISO 20022 will bring important changes for all players across the payment chain. Melissa Tuozzolo, head of payments financial market infrastructures and industry initiatives at Citi Treasury and Trade Solutions likewise noted the need to “operate in both ISO and MT environment as the transition takes place across the world”. Tuozzolo also foresees that emerging technologies such as artificial intelligence (AI) and machine learning (ML), coupled with new data standards will align cross-border payment experience with expectations of ‘new economy’. “The ISO migration could be the catalyst for a 100% STP payments ecosystem—reducing costs and increasing speed, especially in the e-commerce and marketplace business space”, she added.

Melissa Tuozzolo

Head of payments, FMI and industry initiatives,

Citi Treasury and Trade Solutions

So Lay Hua

Group head of transaction banking,

UOB.

As cross-border payments are constrained by inconsistent and unstructured data, the adoption and assessment of the impact of adoption becomes even more critical. Data from SWIFT shows that nearly 10% of FI payments require manual intervention when processing an international payment. Thus, moving to better quality, structured data would bring increased automation, faster processing, effective reconciliation and improved financial risk reporting.

In light of the above, UOB observes that the adoption will drive end-to-end change impacting its channels, payment processing and screening capabilities. To cushion any impacts on customers and partner banks during the adoption phase, it will take a phased and holistic approach. “We will be taking a phased and holistic approach to improve compatibility between our platforms to realise benefits of rich messages whilst minimising impact to clients and partner banks”, elaborated So Lay Hua, group head of transaction banking at UOB.

Wells Fargo sees STP improvements and transaction screening and monitoring as two main areas of longer term impact. “For both of these areas, unstructured data is a barrier to increased efficiency and results in repairs, an inquiry back to the sender, manual reviews and ultimately a delay in the payment execution”, said Michael Knorr, head of payments and liquidity management, Wells Fargo.

Michael Knorr

Head of payments and liquidity management,

Wells Fargo

The core of ISO 20022 adoption is the backend payments engine that consumes and produces the message format and enables end-to-end processing and communication with other enterprise services. The fundamental impact will revolve around decommissioning or combining multiple engines into a single, high-performing engine.

Instant payments catalysed by COVID-19 makes the adoption of ISO 20022 more critical

FIs and their payment businesses are under intense pressure from competing incumbents, new entrants and regulators turning up the heat on compliance, security and transparency. Amid such an environment, the need for better quality data in cross-border payments is now greater than ever. ISO 20022 offers the path to better quality data as its repository holds around 750 business components and more than 1900 message definitions. “Regulators, payment providers and SWIFT have recognised that legacy payment formats may not carry the increased fields and data supported by ISO20022, therefore planned migrations both for cross-border and individual payment schemes are now in progress”, said Bajaj.

Modern payment standards prioritise richness of data over message size and introduce new elements to enhance the scope of messaging. As payment use cases have become more complicated, the existing MT standard is not deemed fit anymore to tackle the current needs of international payments. “The implementation of a more modern payment standard such as XML, JSON was seen as a better platform for future innovation”, suggested Knorr.

The case for enriched data becomes even stronger in case of cross-border payments which are constrained by fragmented and poor information. The ISO 20022 standard will help mitigate frictions by capturing more details in the payment messages, thereby increasing interoperability across cross-border payment systems. “As banking ecosystem undergoes transformation with shifting customer expectations, new payments standards should support the removal of friction and inefficiencies in domestic and cross border payments”, argued Tuozzolo.

To avoid fragmentation in the implementation process of ISO 20022, the industry has created two groups to work on implementation guidelines. The High Value Payments Plus (HVPS+) group provides a forum for the payment system operators to cooperate and agree on a common approach while the Cross-Border Payments and Reporting (CBPR+) group addresses these needs for cross border payments among the banks.

SWIFT continues to support the community through the creation of ISO 20022 programme in cross-border payments and reporting. It is collaborating with a subset of the Payment Market Practice Group (PMPG), defining CBPR+ usage guidelines and translation rules. “The main driver continues to be SWIFT – the global body steering the migration in the correspondent banking space and the market infrastructures (MIs) responsible for the world’s major currencies”, commented Raju.

SWIFT also launched its new in-flow translation service which translates rich ISO 20022 messages into the existing MT format. This service is particularly useful for banks yet to be ready to process ISO 20022 messages. This way, all FIs on the SWIFT network can continue to transact as normal during the industry’s migration phase from November 2022 onwards.

With ISO 20022 benefits, banks can win customers and gain market share

Not only does better data bring enhanced benefits to automation and processing, it provides informed insights, innovation and ability to offer new, value added services in the context of payments. Accurate, complete and standardised data can help save costs by simplifying internal processes as well as fulfilling more stringent AML reporting requirements. All of these translate to better efficiency, improved corporate service experience and opportunities to capture greater wallet share.

“By supporting richer and more structured payment attributes, the industry will benefit from greater transparency, stronger screening standards, better automation, and faster STP processing. This provides customers end-to-end visibility and reconciliation through better data quality”, enumerated So.

“The corporate customer experience is greatly enhanced owing to automated reconciliation of payments, payment tracking and detailed intraday reporting” added Raju.

Moreover, as ISO 20022 supports same rich information such as high quality remittance data for ultimate debtor (customer) and creditor (beneficiary), the adoption is crucial for multinational corporate treasuries that operate shared ‘on-behalf-of’ payment and collection (POBO and COBO) structures.

“Reconciliation automation for ultimate beneficiaries will increase visibility on cash flows and reduce exception handling to support business flows such as POBO and receivable on behalf of (ROBO), added Knorr. Corporates are able build additional efficiencies into their payment processes by facilitating more “just in time” payments and real-time treasury management. “The increased data fields in ISO messages will allow for easier reconciliation of PoBo and RoBo payments”, reported Tuozzolo.

Since its inception, ISO 20022 has been adopted in domestic payment rails in over 70 countries. While ISO 20022 is primarily focused on high value payments infrastructure, there is an opportunity for better harmonisation across all payment types to develop globally-accepted standards for items such as purpose of payment codes, digital identity, etc.

“The migration will allow for structured, unified standards with the end goal of increasing interoperability, STP and improved reconciliation across the payments chain”, said Tuozzolo. “The adoption will create ecosystem connectivity by integrating different payment instruments into one format, offering a consistent syntax for developers for message and API-based solutions”, added Knorr.

An important use case that stands to benefit the entire industry is the enhanced ability to perform more comprehensive checks on a payment. In this process, intermediary institutions are able to identify potential errors and remediate payments without manual intervention before they are passed on to the next bank in the chain. This decreases the potential for payment return/rejects. “The adoption finds emerging use case in regtech as the highly structured nature of the ISO field will allow institutions to better identify payments of true sanctions or AML concerns versus a false positive”, highlighted Tuozzolo. “It will provide better payment intelligence in areas of suspicious activity monitoring, least cost routing and agent monitoring”, also added Knorr.

Structured formats with consistent field usage and improved data parsing through ML will power uniformity and efficiency. “For banks, this means taking on more value added services around enriched reporting, automated investigations and data driven services”, commented Bajaj.

Few challenges stand in the way of ISO 20022 readiness

The journey towards ISO 20022 migration presents challenges which cannot be resolved overnight. Delayed implementation timelines across different markets, budget constraints, co-existence of various formats and existence of several parallel local PMI ISO migration programmes are few notable ones. With ISO set to become the de facto standard for payment messaging by 2025, the migration is a question of “when” rather than “if”.

“With many parallel local PMI ISO migration programs also underway, banks have to balance the ISO migration with other business priorities with a clear strategy and roadmap while ensuring there is alignment in data sets across regions and countries”, highlighted So.

There are also important differences between the implementation guidelines for different payment schemes such as for HVPS+ and CBPR+. The caveat is that the co-existence of multiple formats and various degree of readiness for processing will create challenges for the community. “Banks will need to maintain legacy infrastructure to process MT through FIN while also implement new services to process ISO through FINplus for CBPR+ that migrate to ISO”, argued Bajaj.

“With the complexity of understanding ISO 20022 as a new business standard, addressing differences in specifications of different market infrastructures and SWIFT during the co-existence phase becomes a crucial challenge”, added Raju.

The flexibility of adoption is also leading to slightly different interpretations of “ISO” across market infrastructures. “Different interpretations require additional development efforts for market participants which reduces interoperability and increases inefficiencies”, further said Tuozzolo.

From a regulatory compliance perspective, managing and storing new, additional transaction information while retaining old data also poses challenges. The change to new format means outright downstream impacts; for example, complexities in reporting, additional costs of analytics and data storage. “One of the challenges present is the number of systems and applications that this change impacts including data reporting, storage and various payments initiation options”, highlighted Tuozzolo.

FIs are still attempting to fully grasp the magnitude of the impact on internal systems and operational processes. Moreover, the pandemic is forcing banks to further stretch their IT resources on ensuring business continuity and supporting immediate customer needs. Therefore to support migration as smoothly as possible, it is important to understand the extent of funding that commensurate with proper infra planning. “Banks need to start early to map out the future state, do a front-to-back review of platforms and processes, create programs and obtain funding”, recommended Knorr.

Amount of technical investment to drive adoption will vary by institution

A bank migrating to new messaging standard must consider the costs of maintaining both legacy and new compatible systems, along with expenditures on re-designing of platforms and operational processes to capture ISO compatible data. “Harnessing the richness of ISO will require changes to back end systems (e.g. DDA platforms) to be able to capture structured address data elements”, noted Bajaj.

Investments involved will be determined by a host of factors, including the institution’s current architecture, expected scale of transformation, number of participatory business processes, geographic scope etc. A study commissioned by the UK Payments System Regulator estimated in the case of Single Euro Payments Area (SEPA) ISO 20022 program that for payment service providers (PSPs), migration costs were typically 70% of their annual payment processing costs. The study also estimated the total transition costs to the SEPA Regulation at $13.9 billion, of which two thirds of costs were attributed to ISO 20022 XML adoption.

“Naturally, an institution that participates through subsidiaries in multiple ISO-ready HVPS will have a higher investment requirement than a bank in a country with a HVPS that is not migrating to ISO 20022”, said Knorr. This will be driven by the infrastructure that a bank has already in place, the number of business processes that participate in the payment processes and geographic scope of the bank, he added.

The amount may also vary based on the end goal of the bank. This may be to meet certain regulatory requirements or driving end-to-end payment modernisation. “The amount of investment required will vary based on the extent of benefits that the banks would want to reap out of it. This change can range from the regulatory slice of readiness to supporting end-to-end transformation”, reported So.

Due to the historical limitations of MT messages in cross-border payments, technology which supports the new standards needs to be updated to “open” fields to align to CBPR+/HPVS+ ISO standards. “Therefore, the amount of expected technical investment required will vary from bank to bank based on their current state architecture, and on the age and capabilities of their current technology stack”, pointed So and Tuozzolo. “Successful migration will require multi-year funding as the entire cash ecosystem needs to be enhanced over the next 3 to 4 years”, concluded Raju.

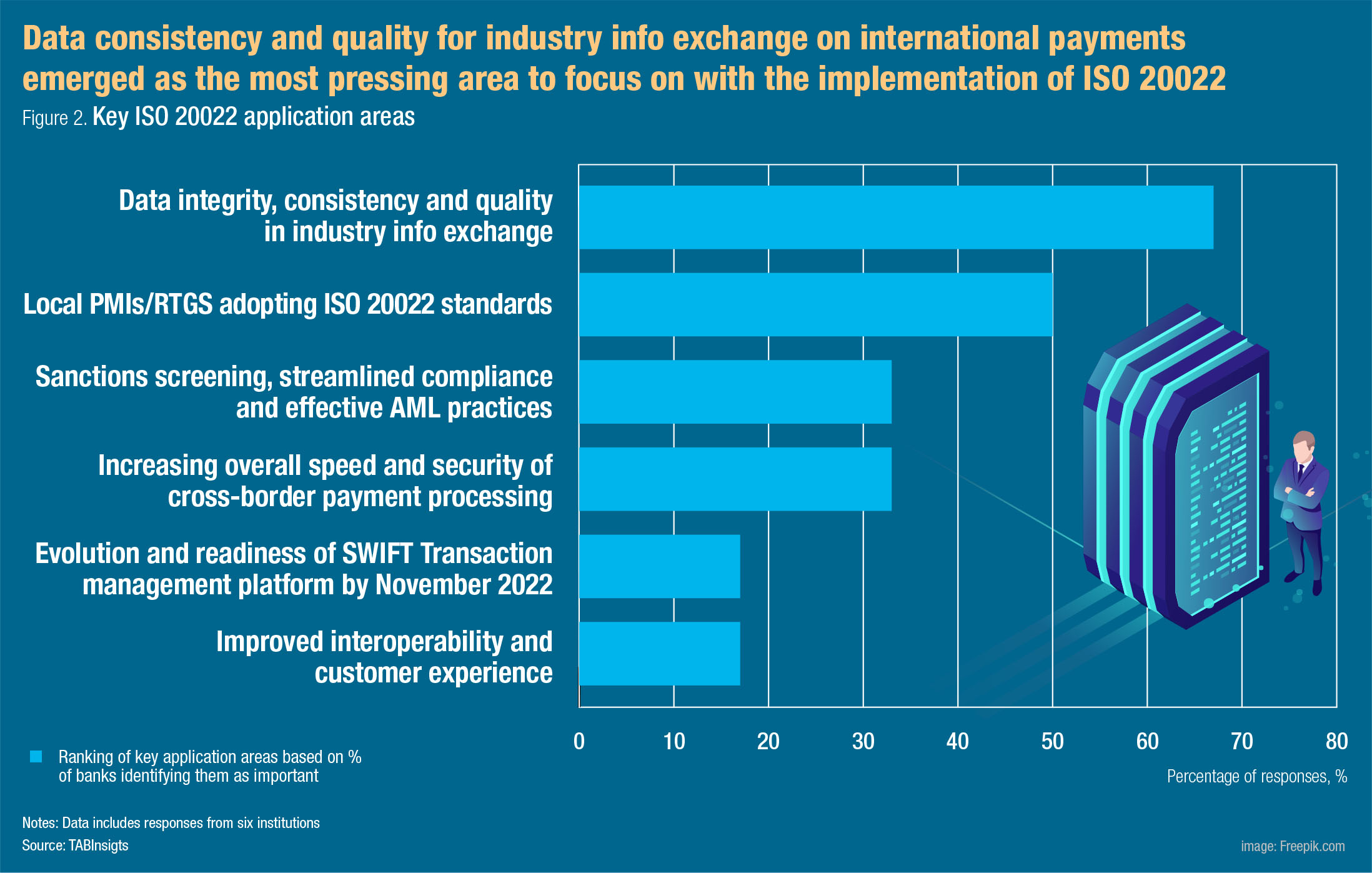

Consistency and quality of industry data exchange emerged as the most pressing application of ISO 20022 migration

Based on TABInsights survey on “one application/area where a FI finds the implementation of ISO 20022 most pressing”, 67% respondents reported that for effective industry information exchange on cross-border payments- data consistency and quality was paramount. Truncation and loss of data due to limitations in current payments standards were identified as a major pain points.

With the migration to ISO 20022, the industry will be able to move towards more efficient screening aimed at reducing number of false positives. This will have a net impact of increasing the overall speed and efficiency of cross border payments, as 33% respondents noted.

There are local PMIs that are still on MT will continue to be on MT beyond November 2022. The final domestic leg of a cross-border payment through these clearing can result in information loss. Therefore, 50% respondents also noted that the adoption of ISO 20022 standards by local PMIs was equally crucial.

Benefits of rich standards only to be fully unlocked on wider adoption

The essential aim and benefit of the ISO 20022 implementation is it ensures the mass adoption and migration of the standard by the whole industry and every bank and FI is compelled to participate. In this sense, better payments data cannot be achieved by any one institution alone; it must be adopted in a coordinated way across the payments ecosystem. Players across the ecosystem must be willing to rethink their operating model, which will require a strong focus on interoperability, data quality and integration of new technologies. “The benefits of ISO- transparency, flexibility, richer data and visibility into customers will only be fully unlocked with wider adoption across the industry”, concluded Tuozzolo.

Support from numerous usage guidelines such as ISO roadmap and CBPR+ market practice, development of new SWIFT tools such as the Transaction Management Platform (TMP) and comprehensive translation solutions will aid in smoothly navigating the transition. “This will be a concerted effort by SWIFT, system vendors, and the large correspondent banks”, added Knorr.

The advent of ISO 20022 is now firmly on the horizon and each institution, whether a global bank, regional player or corporate prepping for minor infrastructural changes, must plan their journey to move in the right direction. All FIs must fully migrate to ISO by November 2025 as MT categories 1, 2 and 9 will be decommissioned for cross-border payments. “During the transition, banks must act as ‘trusted partners’ and continue to support both legacy format and ISO 20022 standards”, noted Bajaj.

.png)

.webp)