- mBridge project has run a six-week pilot participated by over 20 commercial banks

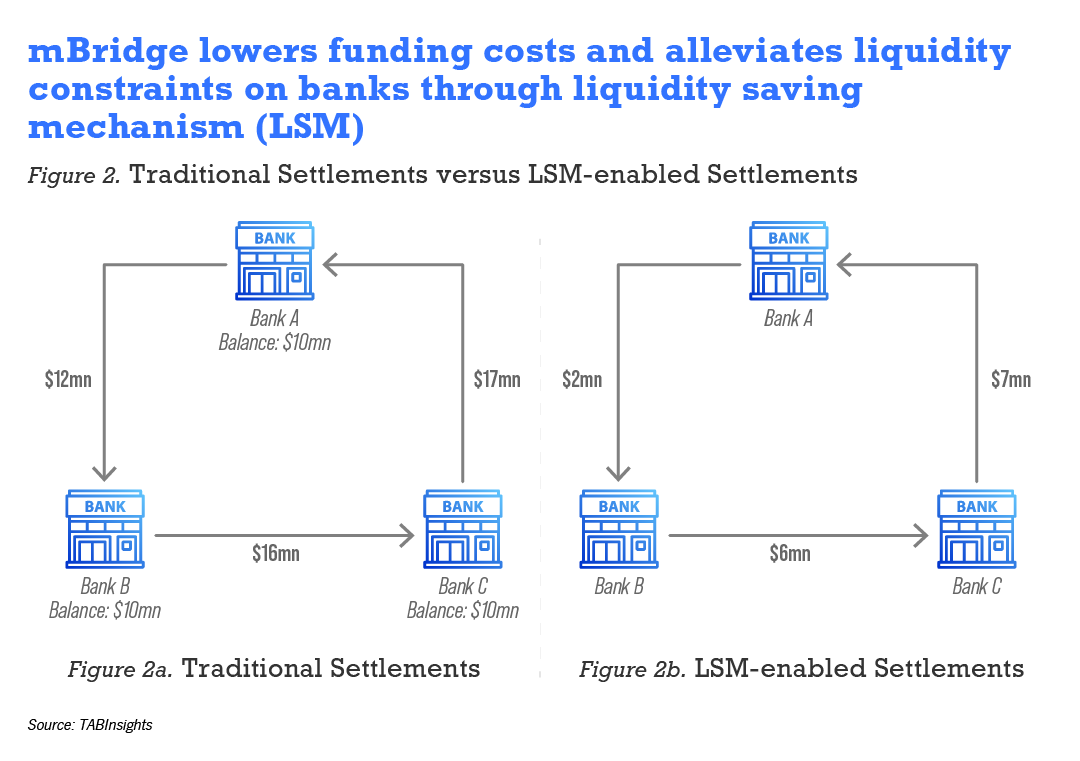

- Tools like liquidity saving mechanism (LSM) and DLT help address pain points in cross-border payment system

- Providing a roadmap for next-generation cross-border settlements

The mBridge pilot, a collaborative project between BIS Innovation Hub Hong Kong Centre (HKC) and four participating central banks to experiment cross-border payments has shown a roadmap for the next-generation cross-border settlement system based on central bank digital currencies (CBDCs) and distributed ledger technology (DLT).

mBridge has overcome the common pain points in existing cross-border settlement systems, such as lengthy, redundant chain of compliance checks, limited trading time, unautomated procedures and low level of data governance. It opens more possibilities for building an economical and faster cross-border payments and settlement system.

mBridge project has run a six-week pilot participated by over 20 commercial banks

The six-week pilot, from 19 July to 23 September, enables banks to get acquainted with the DLT-based platform and ensure smooth operations in the future.

Over 20 financial institutions (FIs), primarily commercial banks in mainland China, Hong Kong, Thailand, and United Arab Emirates (UAE) took part in the pilot. mBridge is by far the largest cross-border CBDC pilot, with over $12 million of CBDCs issued onto the platform, over $22 million of payments and foreign exchange payment versus payment (FX PvP) instantly settled across borders and it has the greatest number of direct pilot participants.

Yi Gang, Governor of the People’s Bank of China (PBoC) said, PBoC is “closely working with Hong Kong Monetary Authority (HKMA) and other monetary authorities on CBDC”, mainly on the most recent mBridge pilot project. He shared his thoughts on the latest developments of CBDC at the Hong Kong FinTech Week on 31 October 2022.

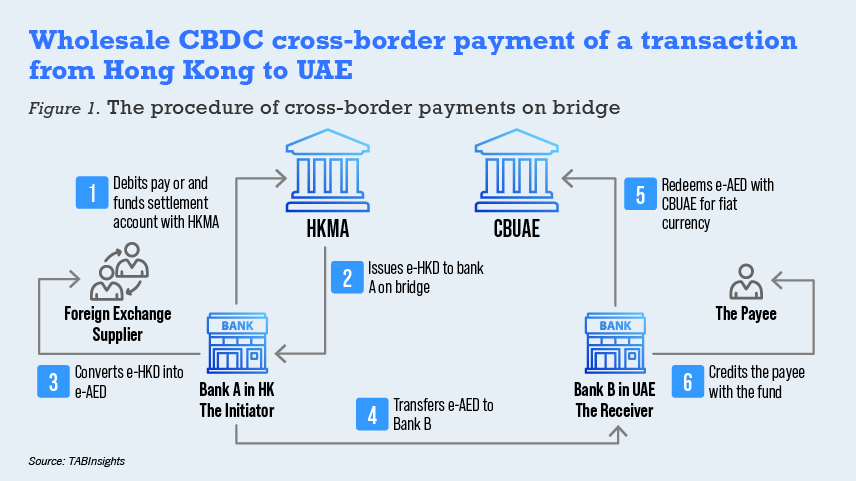

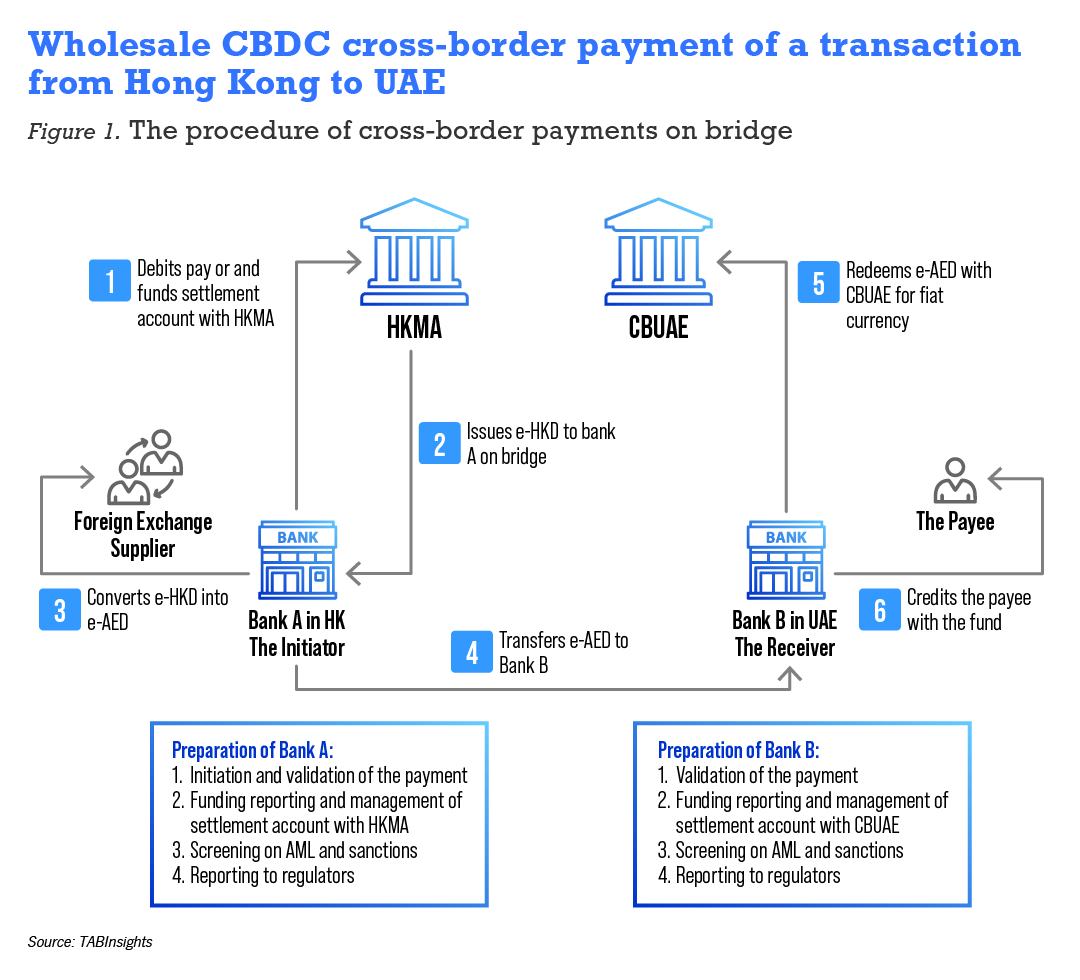

A joint project, mBridge advances the goal of an immediate, secure, economical and universally accessible settlement medium. It is hosted by the BIS Innovation HKC, and four participating central banks in Asia and the Middle East – the Hong Kong Monetary Authority (HKMA), the Bank of Thailand (BOT), the Central Bank of the United Arab Emirates (CBUAE) and the Digital Currency Institute of the People’s Bank of China (PBCDCI).

Tools like LSM and DLT help address pain points in traditional settlement systems

mBridge can facilitate 15 business scenarios from supply chain finance to capital market transactions. The most important and widely applied is cross-border payments and settlements. Conventionally, commercial banks leverage tools and infrastructure such as the real-time gross settlement (RTGS) and Swift/ Clearing House Automated Payment System (CHAPS) for international transactions, which now turn out to be too complex in processing compliance checks along a prolonged time-exhausting transaction chain. Also, cross-border payments are still processed at the domestic clearing branches in the domestic time zones, by and large limiting the trading and operating time.

Cross-border payment settlements nowadays heavily depend on the available cash flow, which means banks need to bear the costs, as this will add to the liquidity constraints. Yet high costs, limited time, and rather lower speed of transactions are relatively less important reasons to aim for a better settlement system. There have been other solutions such as value-day approach, where banks need to clear net in-and-out flows before funding Nostro or settlement accounts, or the liquidity saving mechanism (LSM), which runs parallel with RTGS and decrease the amount of liquidity required to settle the transactions by cancelling the repetitive cash flows.

LSM is a simple but powerful tool installed within mBridge. The pilot also enables the central banks to supervise and review all the liquidity and funding models. LSM can be more effectively leveraged to lower the costs for CBDC cross-border payments.

Huang Jinyue, general manager, digital currency task force at Bank of China Hong Kong (BOCHK) said during the technical pilot testing that BOCHK carried out prototype verification of e-CNY liquidity provision solutions and worked with customers to verify the foreign exchange transaction function between different CBDCs.

In the digital age, most of the data coming through traditional cross-border payments are still limited and unstructured, which forbids regulators to act on sanctions and compliance issues fast or formulate any data-driven insights. Current infrastructures cannot handle advanced data governance measures. With the mBridge pilot, CBDCs are designed with full traceability on the blockchain, and every data point is documented in the transaction log in a unified and standardised form. It is easier for the regulators, and commercial banks trading day in and day out to fully activate their un-excavated and long-neglected data.

DLT also addresses other issues like limited time windows and the exhaustive transaction chain. On the blockchain, there is a DLT smart contract function that allows CBDCs for a higher level of automation and to be more event-triggered. The banks on the bridge get to provide 24x7 real-time cross-border payments with finality to their customers, and such efficiency wins people over.

DLT, being a decentralised tool in its essence, also connects transacting partners point-to-point, which can significantly reduce the redundancy and costs lost to all the onboarding, monitoring, and operating procedures. The DLT-based mBridge is far more friendly to the banks as well as customers.

You Yi, deputy general manager of Bao-Trans Enterprises, a corporate customer in the pilot, said Bao-Trans among many other corporates have experienced first-hand, how using CBDCs on bridge can increase the efficiency of international trade flows. It enables corporates to process cross-border trade and payments efficiently and in a more reliable way.

Providing a roadmap for next-gen cross-border settlements

As Yi Gang said, “privacy protection is one of the top issues on our agenda” at PBoC and its partners. Currently all the sensitive, private, and classified data are still stored off-bridge and managed by the corresponding jurisdictions and shared only on a need-to-know basis.

When coming on bridge, the data will be properly encrypted. A shared blockchain across borders still brings about considerations on data privacy and security. For instance, mBridge still leverages a single-cloud strategy, a rather centralised approach than a decentralised one, and raises some security concerns. The pseudo-anonymity function now used on bridge can protect users by sharing encrypted data only with transacting parties and the respective central banks. More work needs to be done after the pilot, especially on different data privacy and government regulations across jurisdictions.

The next steps for mBridge would be merging the cross-border infrastructure with domestic payment systems and making it more interoperable, and hence applicable to more scenarios and business cases such as migrating the foreign exchange price discovery mechanisms from off-bridge to on-bridge and saving the time spent on communicating about prices on-and-off-bridge. It involves more jurisdictions and participating banks in the project, especially those players from the private sector, to see if they can further spur innovations based on their needs.

CBDCs are expected to have full potential in a digitalised world. Noel Quinn, CEO of HSBC Group said, “In the near future, CBDC payments can lower the costs when looking at it through the banks’ lens.” CBDC could be a significant game changer in delivering fiscal and monetary policies and stimulating demand. To fully realise those potentials, tech-driven infrastructures such as the mBridge project still need to further iterate and evolve.

.png)

.webp)