- In nine of the 26 markets under review, neo-banks or digital-only FIs outperformed commercial banks in digital user growth per month

- The top growth players in the respective categories are Wechat Pay (platform), ICBC China (domestic commercial bank) and Citibank (global commercial bank), Webank China (neo-bank) and ING Group (digital-only bank)

- There has been a rapid increase in the growth in digital users per month among some neo-banks and payments platforms since the beginning of 2018

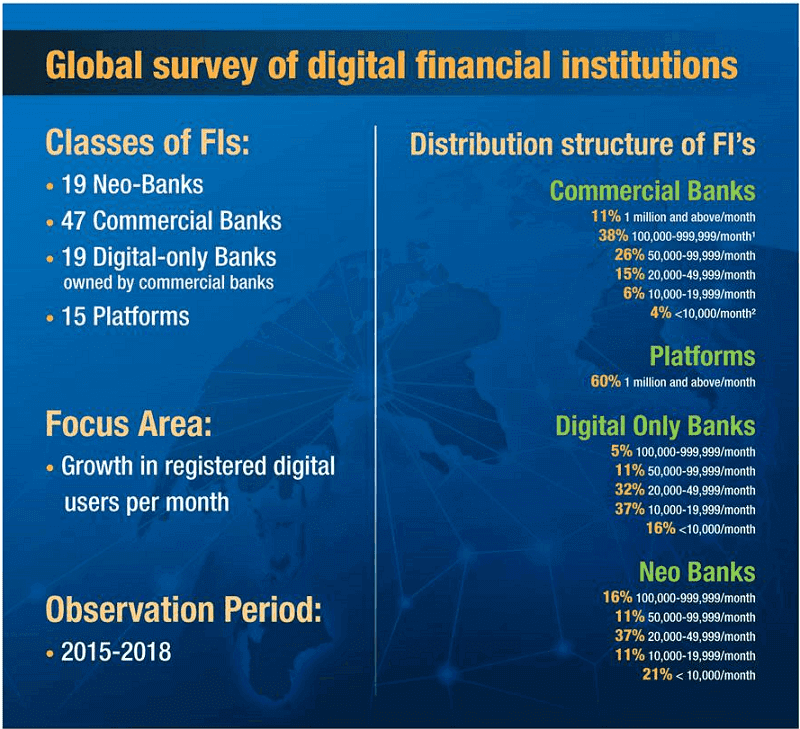

In a global survey which assessed 100 financial institutions across 26 key markets on how well they performed in regards to the growth of digital users per month . Asian Banker Research compared top-tier commercial banks with three other categories of financial institutions, ecommerce/payments/marketplace platforms, neo-banks and digital-only banks set up by commercial banks.

In China, Vietnam, Korea , Japan, India, Brazil, Spain, Germany and the UAE, neo-banks or digital-only FIs outperformed commercial banks in digital user growth per month. However, top tier commercial banks in six out of ten markets such as the US, Canada and Australia continue to outperform neo-banks or digital-only FIs in acquiring and retaining digital customers, with their high-touch high-tech distribution strategy.

Overall, Chinese financial institutions and banks, and global platforms achieved the highest five-star rating with growth of more than one million digital users per month.

Commercial banks’ digital users grew slower in 2018

For domestic commercial banks, 2015 to 2017, was a key period in digital user conversion and growth. We however observed that since 2018 many have seen decelerating digital user growth.

On the contrary, global or regional operating commercial banks inched further up in digital user growth since beginning of 2018 compared to the period between 2015 and 2017.

Santander and BBVA further increased their growth in digital users per month by 32% each in the first half of 2018 compared to the period January 2016 to December 2017. By contrast, Citibank Global outgrew its peers with growth of at least 400,000 digital active retail customers per month between July 2016 and December 2017, it saw a dramatic drop in the first six months of 2018. It grew by only 150,000 new users per month.

Platforms dominate in the category of more than one million digital users per month

Graph 1: Overview of global survey of financial institutions on growth of digital users

Note:

(1) Represents mainly global or large multi-regional banks.

(2) We observed that most first tier commercial banks from smaller countries such as UAE grew their digital user base between 5,000 and 10,000 per month for the period 2016 to 2017. In city-states such as Singapore and Hong Kong commercial banks grew their digital user base between 10,000 and 19,999 per month for the same period. Those were not included. Hence, 4% and 6% present an underestimated figure for this category.

Source: Asian Banker Research

The growth of payments and money transfer platforms

The largest jump in 2018 in digital user growth was Transferwise. It was able to grow its digital user base from January to September 2018 by 167,000 per months as compared to 24,000 users per month in period from January to December 2017. It took Transferwise seven years to reach two million digital users, while it took only nine months in 2018 to double this number.

International payments and money transfer companies such as Transferwise and WorldRemit have breached the ceiling of acquiring more than 100,000 users per month in 2018. According to WorldRemit, over 100,000 digital sign-ups per month were added in September 2018, with a maximum growth of 125,000 in May this year. It crossed the 70,000 users/months in July 2017. Between July 2016 and July 2018 digital sign-ups grew by 124%.

Based on industry data, Apple Pay grew its global customer base from January 2015 to December 2017 by 3.5 million users per month. Between January 2018 to August 2018 it added 15.6 million new digital users per month.

38% of commercial banks achieved a four-star rating

In our survey, 41% of commercial banks grew their digital user base by between 20,000 and 99,999 per month, while 38% of them, mainly representing global or large regional banks achieved a four-star rating by growing between 100,000 and 999,999 digital users per month. Among them are Citibank, Santander, BBVA and a series of commercial banks in large markets such as India, Brazil, US some African countries, Thailand and South Korea. JP Morgan Chase is currently the fastest growing commercial bank in the US and Kasikornbank Thailand outperformed all of its peers based on country population. The survey also found that HSBC and Standard Chartered are no longer the global digital powerhouses they once were in the first decade of the 21st century with HSBC only achieving a two-star rating.

Neo-banks struggle to scale but some shine

Sluggish growth appears to be affecting neo-banks. The large majority of them in mature markets are struggling to achieve scale, and they are often those with a single market focus. In our listing, 21% of all neo-banks obtained a zero-star rating which is defined by a digital user growth of less than 10,000 per month, making them vulnerable to potential acquisition or merger by commercial banks. 48% of neo-banks achieved a one- or two-star rating growing between 10,000 and 49,999 users per month. A few neo-banks in Europe and the US have seen a dramatic rise in digital users since the beginning of 2018 in particular Revolut, N26 and Monzo in Europe and Chime in the US. Revolut has seen the most significant rise in digital user growth per month. From July 2015 to October 2017 it added on average 34,000 digital users per month. This increased in line with their global expansion to 157,700 digital users per month for the period from November 2017 to November 2018. Revolut is the only neo-bank, together with Marcus in the US, which achieved a three-star rating.

Digital-only banks saw mixed results in digital user growth per month

Only two digital-only banks run by commercial banks, Digibank India by DBS (Asia) and BankMobile, a division of Customers Bank (US), achieved a three-star rating, while ING Group (Global) was the only digital-only bank that achieved a four-star rating. 53% of financial institutions in this category grew by less than 19,999 users per month. However, if we standardise digital user growth per month based on country population, Liv by Emirates NBD in the UAE is the best performing digital-only bank followed by ING Direct in Australia.

Platform players dominate list of top digital financial institutions

Table 1 Growth in digital users per month (#)

| FI Category | Country | One Million and above |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Platform | China | WeChat Pay | 18,548,000³ | 13.38 | Jan 2015- Jun 2018 |

| Platform | China | Alipay | 9,200,000³ | 6.64 | Jan 2015- Dec 2017 |

| Platform | Global | Apple Pay | 5,705,000¹ | n/a | Jan 2015- Aug 2018 |

| Platform | India | Paytm Payments Bank | 5,600,000³ | 4.18 | Jan 2014- May 2018 |

| Commercial Bank | China | ICBC | 3,750,000³ | 2.70 | Jan 2016- Dec 2017 |

| Commercial Bank | China | China Construction Bank | 3,458,000² | 2.49 | Jan 2016- Dec 2017 |

| Commercial Bank | China | Agricultural Bank of China | 2,750,000³ | 1.98 | Jan 2016- Dec 2017 |

| Platform | Global | PayPal | 2,044,000¹ | n/a | Jan 2015- Sept 2018 |

| Platform | India | Google Pay (formerly Tez) | 2,000,000¹ | 1.49 | Sept 2017-Apr 2018 |

| Neo-Bank | China | Webank | 1,670,000 | 1.20 | Jan 2015- Dec 2017 |

| Platform | Global | Samsung Pay | 1,292,000² | n/a | Jan 2016- Dec 2017 |

| Commercial Bank | China | China Merchants Bank | 1,175,000³ | 0.85 | Jan 2016- Dec 2017 |

| Commercial Bank | China | Ping An Bank | 1,167,000² | 0.84 | Jan 2016- Dec 2017 |

| Platform |

Multi Regional |

LINE Pay | 1,048,000 | 2.17 | Jan 2015- Jun 2018 |

| Platform |

China/ Hong Kong |

Welab | 1,044,000 | 0.75 | July 2016- July 2018 |

| FI Category | Country | 100,000-999,999 |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Commercial Bank | India | State Bank of India | 870,000³ | 0.65 | Jan 2016- Dec 2017 |

| Commercial Bank | China | China CITIC Bank | 583,300² | 0.42 | Jan 2016- Dec 2017 |

| Neo-Bank | Korea | Kakao Bank | 523,300 | 10.17 | July 2017- July 2018 |

| Platform | China | Lufax | 467,500 | 0.34 | July 2017- Jun 2018 |

| Commercial Bank | Global | Citibank | 397,000? | n/a | July 2016- Jun 2018 |

| Commercial Bank |

Multi Regional |

Santander | 390,000 | 0.46 | Jan 2016- Jun 2018 |

| Commercial Bank |

Multi Regional |

BBVA | 383,300 | 0.56 | Jan 2017- Jun 2018 |

| Commercial Bank | US | JP Morgan Chase | 290,300¹ | 0.89 | Jan 2016- Jun 2018 |

| Platform | Vietnam | MoMo | 270,600³ | 2.83 | Jan 2016- Oct 2018 |

| Platform |

Multi Regional |

M-PESA | 222,200³ | 0.14 | Jun 2015- May 2018 |

| Commercial Bank | Nigeria | First Bank of Nigeria | 210,600 | 1.10 | Jan 2016- Dec 2017 |

| Neo-Bank | Brazil | NU Bank | 208,300 | 1.00 | Oct 2017- Sept 2018 |

| Commercial Bank | Thailand | Kasikornbank | 203,300³ | 2.94 | Jan 2016- Jun 2018 |

| Commercial Bank | India | ICICI | 194,400 | 1.45 | Jan 2015- Dec 2017 |

| Neo-Bank | China | Mybank | 190,300 | 0.14 | Jan 2015- Oct 2017 |

| Commercial Bank | Brazil | Banco Bradesco | 173,300¹ | 0.83 | Jan 2016- Jun 2018 |

| Commercial Bank | Brazil | Santander | 170,000 | 0.81 | Jan 2016- Jun 2018 |

| Commercial Bank | US | Bank of America | 148,100¹ | 0.45 | Mar 2016- Jun 2018 |

| Commercial Bank | Africa | Ecobank | 135,100³ | 0.10 | Jan 2016- Apr 2018 |

| Commercial Bank | Global | Standard Chartered |

110,000- 140,000² |

n/a | Mar 2014- Mar 2017 |

| Commercial Bank | US/Canada | Citibank | 128,600¹ | 0.35 | Oct 2017- Jun 2018 |

| Digital-only Bank | Global | ING Group | 123,300 | n/a | Jan 2016- July 2018 |

| Commercial Bank | Korea | Hana KEB | 116,700³ | 2.27 | Jan 2016- Dec 2017 |

| Commercial Bank | Korea | Shinhan Bank | 113,800³ | 2.21 | Jan 2016- Dec 2017 |

| Commercial Bank | UK | Barclays | 106,300 | 1.61 | Jan 2016- Aug 2018 |

| FI Category | Country | 50,000-99,999 |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Platform |

Multi Regional |

Transferwise | 95,000³ | n/a | Jan 2017- Sept 2018 |

| Commercial Bank | Nigeria | Diamond Bank | 94,400³ | 0.49 | Oct 2016- Mar 2018 |

| Platform | China | Yirendai (CreditEase) | 91,700 | 0.07 | Jan 2017- Dec 2017 |

| Commercial Bank | UK | RBS | 82,300¹³ | 1.25 | Jan 2016- July 2018 |

| Commercial Bank | US | Wells Fargo | 81,250¹ | 0.25 | Aug 2016- Feb 2018 |

| Digital-only Bank | India | Digibank by DBS | 80,000 | 0.60 | Apr 2016- Apr 2018 |

| Neo-Bank | US | Marcus by Goldman Sachs | 76,900 | 0.24 | Oct 2016- Nov 2018 |

| Commercial Bank | Turkey | Garanti Bank | 78,800 | 0.98 | Jan 2016- Sept 2018 |

| Platform |

Multi Regional |

WorldRemit | 77,000 | n/a | July 2016- July 2018 |

| Commercial Bank | Italy | Intesa Sanpaolo | 73,500² | 1.21 | Sept 2015-Jun 2018 |

| Neo-Bank |

Multi Regional |

Revolut | 73,200 | n/a | July 2015- Nov 2018 |

| Commercial Bank | Malaysia | Maybank | 70,800 | 2.24 | Sept2014-Sept 2018 |

| Commercial Bank |

South Africa |

First National Bank | 69,600²³ | 1.23 | Apr 2016- Jun 2018 |

| Commercial Bank | UK | Loyds Banking Group | 62,500 | 0.95 | Apr 2016- Mar 2018 |

| Commercial Bank | Nigeria | Guaranty Trust Bank | 60,000² | 0.31 | Jan 2017- Dec 2017 |

| Commercial Bank | Spain | Caixa | 56,700² | 1.22 | Jan 2015- Jun 2018 |

| Commercial Bank | Taiwan | CTBC | 52,000² | 2.19 | Dec 2016- Dec 2017 |

| Digital-only Bank | US | BankMobile | 50,000 | 0.15 | Jan 2015- Dec 2017 |

| Commercial Bank | UK | Santander | 50,000 | 0.76 | Jan 2016- July 2018 |

| FI Category | Country | 20,000-49,999 |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Commercial Bank | Global | HSBC | 41,700 | 0.01 | Apr 2015- Apr 2018 |

| Commercial Bank |

South Africa |

Capitec Bank | 39,100³ | 0.69 | Nov 2015- Sept 2018 |

| Commercial Bank | Canada | Royal Bank of Canada | 37,000¹ | 1.00 | Jun 2016- Jun 2018 |

| Neo-Bank | Japan | Rakuten Bank | 34,700 | 0.27 | Jan 2015- Dec 2017 |

| Neo-Bank | UK | Monzo | 32,300 | 0.49 | Mar 2016- Sept 2018 |

| Digital-only Bank | Indonesia | Jenius | 32,000 | 0.12 | Aug 2016- Aug 2018 |

| Commercial Bank | Australia/NZ | CBA | 31,200¹ | 1.06 | July 2014- Jun 2018 |

| Digital-only Bank | Germany | ING DIBA | 31,000² | 0.37 | Jan 2016- Dec 2017 |

| Neo-Bank | Brazil | Banco Inter Brazil | 30,300 | 0.14 | Jan 2016- Sept 2018 |

| Neo-Bank | Brazil | Banco Original | 25,800 | 0.12 | Apr 2016- Dec 2017 |

| Neo-Bank | France | Nickel | 25,500 | 0.38 | Jun 2016- May 2018 |

| Commercial Bank | Australia | Westpac | 25,300 | 1.03 | Apr 2016- Sept 2018 |

| Commercial Bank |

ASEAN/ North Asia |

DBS Group | 25,000 | 0.01 | Dec 2016- Dec2017 |

| Digital-only Bank | Japan | Jibun Bank | 24,700 | 0.19 | Jan 2015- Dec 2017 |

| Digital-only Bank | France | Boursorama by Societe General | 24,700 | 0.37 | Jan 2016- July 2018 |

| Neo-Bank | UK/Europe | N26 | 23,800 | 0.03 | Jan 2015- Jun 2018 |

| Digital-only Bank | Spain | imaginBank by CaixaBank | 21,700 | 0.47 | Jan 2016- Dec 2017 |

| Neo-Bank | US | Chime | 21,300 | 0.07 | Jun 2014- Apr 2018 |

| Digital-only Bank | Japan | SBI Sumishin Net Bank | 20,800 | 0.16 | Jun 2014- Dec 2017 |

| Commercial Bank | Japan | MUFJ | 20,000² | 0.16 | Jan 2014- Dec 2017 |

| FI Category | Country | 10,000-19,999 |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Digital-only Bank | Australia | ING Direct | 19,200¹ | 0.78 | Jan 2016- Dec 2017 |

| Commercial Bank | UK | Metro Bank |

16,000- 18,000² |

0.26 | Jan 2016- Apr 2018 |

| Commercial Bank | Spain | Santander | 16,700 | 0.36 | Jan 2016- July 2018 |

| Digital-only Bank | Nigeria | ALAT by Wema | 16,500 | 0.09 | May 2017- Sept 2018 |

| Digital-only Bank | Indonesia | Digibank by DBS | 14,600 | 0.06 | Aug 2017- July 2018 |

| Neo-Bank | UK/Europe | Monese | 14,300 | 0.02 | Sept 2015- Aug 2018 |

| Digital-only Bank | US | Ally Bank | 14,100 | 0.04 | Jan 2015- Dec 2017 |

| Digital-only Bank | Eurozone | Hello Bank! by PNB Paribas | 14,000 | 0.21 | Mar 2016- Jun 2018 |

| Neo-Bank | UK | Starling Bank | 13,100 | 0.20 | May 2017- Aug 2018 |

| Digital-only Bank | Taiwan | Richart by Taishin International | 13,000 | 0.55 | Apr 2016- July 2018 |

| Commercial Bank | Poland | mbank | 10,100 | 0.27 | Jan 2016- Jun 2018 |

| Digital-only Bank | UAE | Liv by Emirates NBD | 10,000 | 1.06 | May 2017- May 2018 |

| FI Category | Country | <10,000 |

Growth in digital users per month |

‰ of total population |

Period of Observation |

|---|---|---|---|---|---|

| Commercial Bank | Baltics | SwedBank | 8,300 | 0.52 | Jan 2017- Dec 2017 |

| Commercial Bank | Spain | BBVA | 6,900 | 0.15 | Oct 2015- Feb 2018 |

| Neo-Bank | Israel | Pepper by LEUMI |

6000- 8000² |

0.80 | Jun 2017- Jun 2018 |

| Digital-only Bank | Germany | Fidor Bank by BPCE France | 5,000 | 0.06 | Jan 2016- Aug 2017 |

| Digital-only Bank | France | Hello Bank! by PNB Paribas | 4,000 | 0.06 | Mar 2016- Jun 2018 |

| Neo-Bank | US | Simple | 3,800 | 0.01 | 2012- July 2013 |

| Neo-Bank | Canada | KOHO | 2,900 | 0.08 | Mar 2017- Aug 2018 |

| Neo-Bank | UK | Atom Bank | 2,100 | 0.03 | Apr 2016- Mar 2018 |

| Digital-only Bank | Canada | EQ Bank by Equitable Bank | 2,100 | 0.06 | Jan 2016- Dec 2017 |

Notes:

(1) active digital users as defined by the FI

(2) estimated based on indirect data such as active ratios, total customer, growth, or retail digital user base

(3) mobile banking users only

(4) According to Citibank reports active digital consumer banking users grew by 337,500 per month between July 2016 and June 2018. Asian Banker Research applied an 85% digital active rate to determine total registered digital consumer banking base.

(5) ‰ of total population is defined as the growth of digital users per month divided by total country population and measured in per mille = 1/1000

(6) To determine ‰ for multi-regional FIs we aggregated the number of population by country.

Global survey of digital financial institutions: Methodology

- The overall objective of this listing is to rank the top-tier digital FIs according to their ability to attract digital users (across all business segments).

- The survey covers key global markets such as the US, South America, Canada, Europe, Africa and the Asia Pacific.

- The survey took into consideration mainly the period from 2015 to 2018.

- The time period for each institution varies slightly but overlap with the core period between 2016 and 2017.

- The listing is not exhaustive. The focus was on the top tier players in key market and region and for those where data were publicly available.

- For the sake of simplicity, the survey defines all digital banks set up by non-bank FIs as neo-banks. For digital banks set up by commercial banks we refer to digital-only banks.

- Data reflect gross onboarding and acquisition figures, not net growth which discounts for attrition.

- Digital users per month are based on the growth of registered digital users which includes internet and mobile only, regardless whether they were directly digitally acquired, in the case of neo banks, platforms or digital banks, or digitally onboarded into mobile and internet banking which often is the case for commercial banks.

- The findings of the survey do not make assumptions about the quality of those accounts in regards to active accounts measured through a certain period or by measuring attrition.

- As for digital-only banks, the data do not tell how many of those onboarded were from the parent bank.

- At times, the reason for the differences in client acquisition per months between digital FIs in the same market is not performance but different market positioning such as in the case of WeBank and MyBank in China. WeBank focuses on individual clients and consumer financing, while Mybank’s target segment is serving Micro and Small Enterprise (MSEs), hence the smaller numbers.

- Star Rating 2018: Based on average growth of digital users per month

.png)

.png)

.webp)