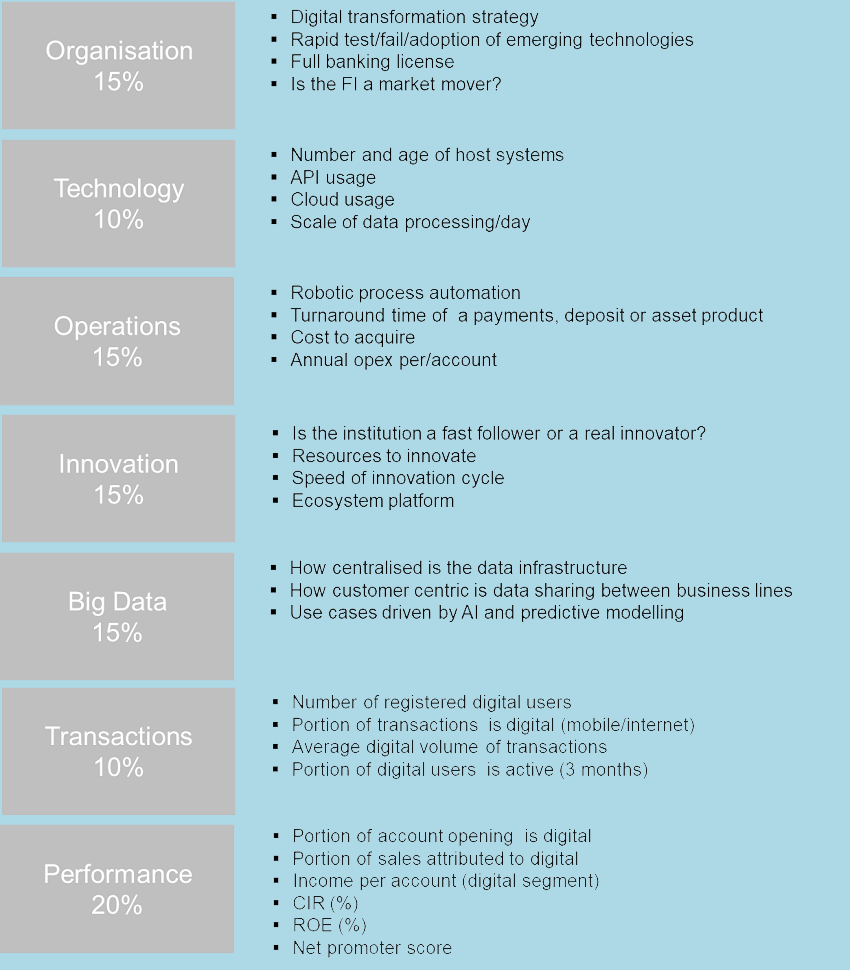

- Asian Banker developed a methodology to track and rate financial institution on their journey to become highly competitive digital players

- Despite progress, the results indicate that, for most commercial banks, their digital capabilities remain too marginal to be competitive.

- Biggest gap between digital plays from Greater China and the rest is found in big data and how they leverage on sophisticated visualisation, augmentation and predictive modelling.

The Asian Banker 2018 ranking of digital retail financial services providers across more than 16 markets in Asia Pacific, the Middle East and Africa reveals that the most competitive digital retail financial institutions come all but from China, and the elite club of the top 10, representing all non-bank financial players, are exclusively from China, Korea and Australia.

“We have developed a methodology to track and rate financial institution on their journey to become highly competitive digital players and how prepared a player is to compete in the digital world,” said Foo Boon Ping, managing editor, The Asian Banker. The ranking takes into account commercial banks, digital only banks, platform based ecosystems and technology companies.

Findings at a Glance

- Ownership - unlike in Europe and the US, more than half of all digital only banks covered in this survey are legal entities of commercial banks.

- Competitive capabilities - despite the progress commercial banks made in moving towards digital main bank, the results indicate that, for most commercial banks, their digital capabilities remain too marginal to be competitive.

- Performance - most digital only banks in Asia, the Middle East face a difficult road as they continue to lack scale and profitability.

- Platform architecture - while digital only plays owned by commercial banks, have separate middle ware and front end user interfaces, they are built on top of a shared core legacy system architecture which continues to be a drag on innovation cycles and faster product development. In contrast, six out of the top 10 in the survey run on financial cloud computing platforms allowing them to set up and operate at a fraction of the cost of commercial banks.

- Cost advantages – better technologies lower the cost of acquisition, annual account cost, but also enables those players to lend money more competitively in the market. In China, the average annual operating cost per account of a digital financial services provider is only 1/10 compared to the best run commercial banks in China, while the cost of acquiring an account is below $0.8. In comparison, the cost of a digital acquisition in commercial banks in mature retail financial services markets in Asia ranges between $50-$80.

- Pricing and revenue models - digital only banks and financial services providers display a wide variety of revenue and pricing models. 4 out of 10 players surveyed shun away from charging overtly for base transaction and rather aim for selling products and services on top of it as a revenue model.

- Transformative technologies - The survey also indicated that the best digital financial services institutions have already launched use cases in the area of transformative technologies such as distributed ledgers, advanced automation, cloud computing, augmented and virtual reality and machine learning.

- Big data and AI - the biggest gap between players in Greater China and the rest is found in Big Data and how their platforms make use of sophisticated visualisation, augmentation and predictive modelling. What sets those apart is the scope of data processing, the availability of large data pools to all relevant parts of their organization and a strategic focus on AI.

Digital transformation or incremental change?

Digital retail financial services providers display diverse network and business models ranging on the network side from pure digital to hybrid online offline or small store agent networks. From a business perspective, the majority starts out with payments, expanding gradually into deposit and wealth propositions. We also noted, that some P2P lenders and platform based ecosystem players in Greater China built cutting edge cross product platforms and now evolving into the next stage of evolution, becoming service cloud platform providers of FaaS (fintech as a service) offering modularised service options for infrastructure, platform and software.

Top digital retail financial services provider

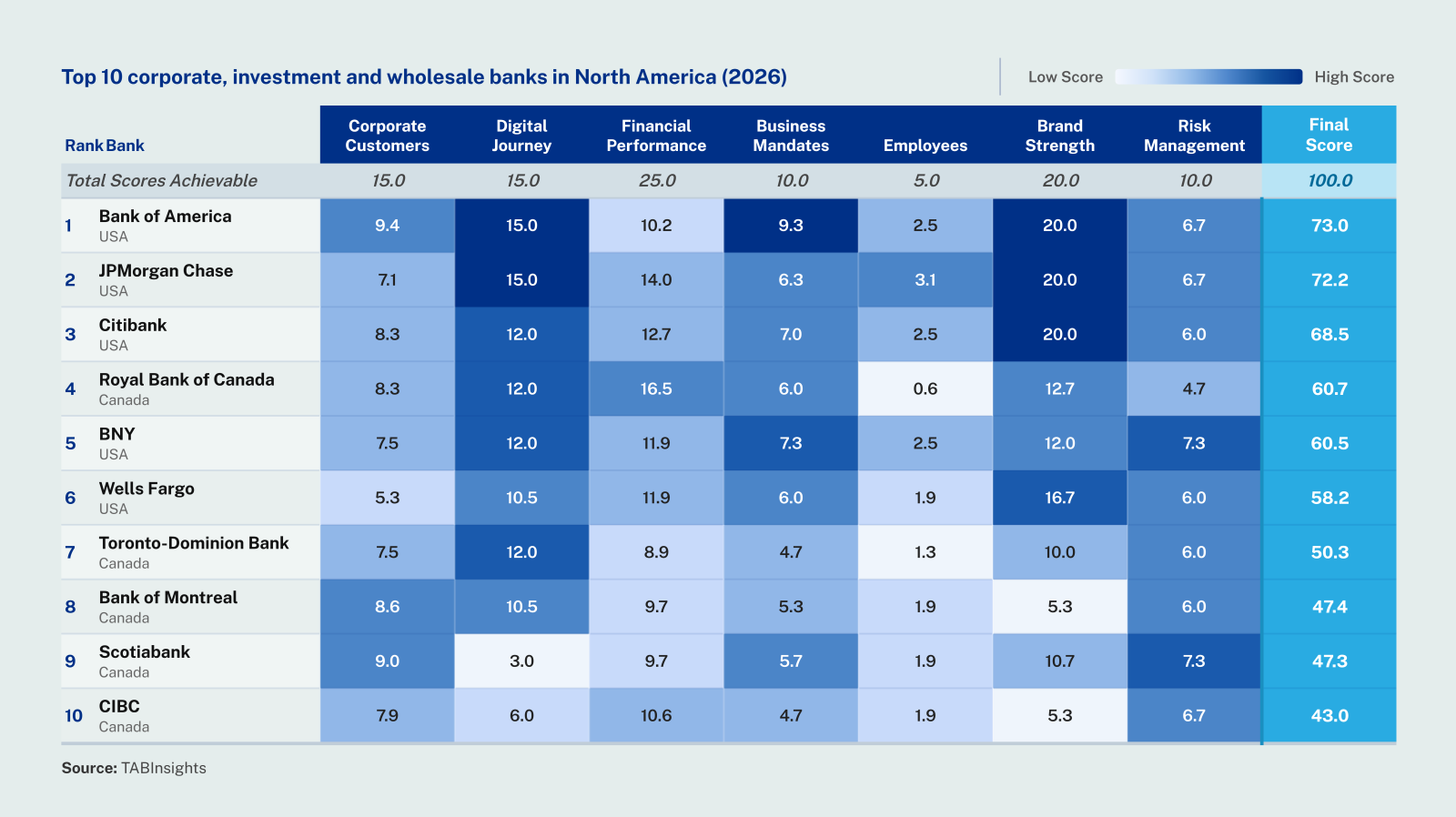

Table 1. Digital Retail Financial Service Provider Ranking 2018

| Bottom Line Impact | Organisation | Digital & Innov | Operations | Big Data & Analytics | Technology | Transactions | Total Scores | |

|---|---|---|---|---|---|---|---|---|

| Weightage | 20% | 15% | 15% | 15% | 15% | 10% | 10% | 100% |

| Max Scores | 10 | 7.5 | 7.5 | 7.5 | 7.5 | 5 | 5 | 50 |

| Ant Financial Services China | 7.3 | 6.1 | 5.7 | 6.5 | 5.5 | 4.8 | 4.5 | 4.5 |

| Tencent Financial Technologies China | 6.8 | 5.8 | 5.4 | 6.5 | 5.0 | 4.8 | 5.0 | 39.3 |

| JD Finance China | 5.0 | 5.0 | 5.0 | 6.0 | 4.0 | 4.1 | 4.0 | 33.1 |

| Kakao Bank Korea | 5.4 | 4.4 | 3.6 | 5.9 | 1.5 | 3.8 | 3.7 | 28.2 |

| WeBank China | 6.0 | 3.9 | 3.0 | 5.3 | 2.0 | 3.9 | 4.0 | 28.1 |

| MyBank China | 5.7 | 3.9 | 2.9 | 5.3 | 2.0 | 4.0 | 3.7 | 27.5 |

| U Bank/NAB Australia | 6.1 | 3.9 | 3.4 | 5.3 | 1.5 | 3.5 | 3.0 | 26.7 |

| ING Australia | 6.3 | 3.9 | 3.2 | 5.0 | 1.5 | 3.2 | 3.2 | 26.2 |

| CBA Australia | 4.2 | 5.3 | 4.2 | 3.0 | 3.0 | 3.8 | 2.6 | 26.1 |

| China Merchants Bank | 5.5 | 4.4 | 3.2 | 4.0 | 2.0 | 3.4 | 3.3 | 25.7 |

| Digibank/DBS India | 4.5 | 4.4 | 3.6 | 2.3 | 1.8 | 4.2 | 2.6 | 23.3 |

| Paytm Payments Bank India | 5.4 | 3.9 | 3.8 | 2.5 | 1.5 | 3.8 | 2.4 | 23.3 |

| ALAT/Wema Nigeria | 4.1 | 4.3 | 3.6 | 2.8 | 1.5 | 3.6 | 3.3 | 23.1 |

| CIMB Malaysia | 4.0 | 4.4 | 4.2 | 2.9 | 1.5 | 3.8 | 1.9 | 22.7 |

| Rakuten Bank Japan | 5.5 | 4.7 | 3.2 | 2.0 | 1.5 | 3.4 | 2.1 | 22.5 |

| Jibun Bank Japan | 4.9 | 4.3 | 3.0 | 2.5 | 1.5 | 3.8 | 2.1 | 22.1 |

| Liv/Emirates NBD UAE | 4.2 | 4.4 | 3.9 | 1.5 | 1.8 | 3.1 | 3.1 | 22.0 |

| CTBC Taiwan | 4.2 | 4.6 | 2.7 | 2.5 | 2.8 | 3.0 | 2.1 | 21.9 |

| Hana Bank Korea | 3.1 | 4.2 | 4.2 | 2.8 | 1.8 | 3.9 | 2.1 | 21.9 |

| DBS Singapore | 3.1 | 5.0 | 3.6 | 1.8 | 2.8 | 3.2 | 2.0 | 21.5 |

| Westpac Australia | 3.4 | 5.0 | 2.1 | 2.5 | 3.2 | 2.6 | 2.5 | 21.3 |

| Richart/Taishin Taiwan | 3.8 | 4.2 | 2.6 | 2.0 | 1.9 | 2.8 | 3.5 | 20.6 |

| O-Bank Taiwan | 4.2 | 4.3 | 2.4 | 2.0 | 1.8 | 2.8 | 3.1 | 20.5 |

| OCBC Singapore | 3.3 | 4.4 | 2.9 | 2.3 | 2.8 | 2.9 | 2.0 | 20.5 |

| ICICI Bank India | 3.4 | 4.9 | 2.3 | 2.3 | 1.8 | 3.6 | 2.0 | 20.1 |

| Citibank Hong Kong | 2.6 | 4.4 | 3.0 | 2.3 | 2.0 | 2.6 | 2.8 | 19.6 |

| FriMi/NTB Sri Lanka | 3.2 | 3.9 | 2.4 | 3.8 | 1.3 | 3.4 | 1.6 | 19.6 |

| Jenius/BTPN Indonesia | 3.3 | 3.1 | 1.5 | 1.8 | 1.0 | 3.3 | 3.3 | 17.3 |

| Standard Chartered Hong Kong | 2.7 | 3.9 | 2.1 | 1.9 | 1.5 | 2.6 | 2.1 | 16.7 |

| Eon/UnionBank Philippines | 2.9 | 3.3 | 1.5 | 1.8 | 1.0 | 3.4 | 2.7 | 16.7 |

| Timo Vietnam | 3.3 | 2.3 | 2.0 | 1.0 | 1.8 | 2.8 | 3.1 | 16.3 |

| Citibank Philippines | 2.3 | 3.6 | 1.3 | 1.6 | 1.3 | 2.7 | 0.9 | 13.6 |

Despite the progress commercial banks made in moving towards digital main bank, the results indicate that, for most commercial banks, their digital capabilities remain too marginal to be competitive. This makes commercial banks vulnerable to lose further share in their core businesses and the next generation of customers.

Responding to the threat, most digital only banks in Asia, the Middle East and Africa emerged in a relatively short period of time since 2016 – but they face a difficult road as they continue to lack scale and profitability. In some instances, the lack of a full banking licence and the absence of e-KYC provides a drag on customer acquisitions. This is in particular prevalent in emerging markets such as India, Indonesia and Vietnam. Some digital experiments failed altogether. Shinhan Bank’s Sunny Bank folded up in 2017 due to lack of distinction between parent platform and digital bank, characterising the challenges banks face to go digital.

Retail financial services are by nature volume businesses where scale drives marginal cost down to a minimum. Hence, digital only banks outside China are at a stage where a premium is put on acquiring customers rather than being profitable, for now at least. Banks in Nigeria, for instance, believe to be profitable one needs to have at least 20 million active digital users. In our ranking out of 20 digital only banks and retail financial services providers only 8 make money, while none of the ones launched since 2016 is profitable yet.

Threshold account numbers certainly depends on a variety of factors such as market conditions and maturity but more so on the technology infrastructure, the products and services offered and the revenue and pricing model. More specifically, the survey found that 4 out of 10 players surveyed shun away from charging overtly for base transaction and rather aim for selling products and services on top of it as a revenue model. This route may take time, however, to monetise the business.

In a traditional bank, the revenue mix consists generally of 1/3 fees and 1/3 interest income. There is some indication, that digital banks that start out with both, payments and interest income, instead of transaction fees only, become faster profitable. For example, in FY2017, kakaobank made a profit of 25 billion won from the margin of its lending and deposit accounts. However, losses recorded due to general administrative spending, including fees and depreciation costs from IT investment created an overall loss of 91.7 billion won, according to its annual report.

Digital is driving down operational cost

Digital retail financial services providers ambitiously aspire to lower their cost to income ratio to 30% in the next three to four years. Most of this will depend on the underlying technology architecture, and how fast they can scale and introduce product and service applications customers are willing to pay for. For example, Kakaobank spent 33% of what a commercial bank would have spent with UNIX when it used the Linux based operating system for its platform. In our ranking, six out of the top ten in the survey are on a financial cloud computing platform

Oversized capital expenditure to set up the full architecture, including initial platform, staffing and licensing costs further contributes to this delayed road to profitability. To better manage this, some players have leveraged on software-as-a-service based technologies to shift high capital expenditures (CapEx) into operational expenditure (OpEx).

In the case of digital-only banks owned by commercial banks, middle ware and front-end user interfaces sit on top of a shared core legacy system architecture which continues to be a drag on innovation cycles and faster product development. On average, digital banks run new product releases and feature updates once every three weeks. In comparison, leading players run between 12 to 40 updates a week.

Operational cost advantages with a lean and open architecture contribute to lower cost of acquisition and account servicing but also to lend money more competitively in the market. ,. In China, the average annual operating cost per account of a digital financial services provider is only 1/10 compared to the best run commercial banks in the country, while the cost of acquiring an account is below $0.8. In comparison, the cost of a digital acquisition in commercial banks ranges between $50-$80.

We observed that automation and straight through processing at the front office was present in 90% of all surveyed digital only banks and financial institutions, but only 23% of all financial service providers deployed a level of back office automation of more than 95%.

Ant Financial has developed a “computer + people” (By using big data and robotic process automation for loan applications, it takes 3 minutes to apply online, 1 second to loan approval and zero human intervention for the entire process

Big Data and AI

The survey also indicated that the best financial services institutions have already launched use cases in the area of potentially transformative technologies such as distributed ledgers, advanced automation, internet of things, cloud computing, augmented and virtual reality and machine learning. Some of those have been extensively deployed. For example, at Kakaobank, more than 90% of processes are based on robotic process automation, while WeBank in China is using blockchain technology for their loan settlement with third party institutions. Ant Financial China also deploys almost 100% of their computational load in the cloud, while AI increasingly drives business applications.

Interestingly, the biggest gap between players from Greater China and the rest is found in big data and how they leverage on sophisticated visualisation, augmentation and predictive modelling. What sets those apart is the scope of data processing, the availability of large data pools to all relevant parts of their organisation, and a strategic focus on AI.

Having the ability to do active profiling and to understand what the customer is trying to do next has become a key competitive advantage, and the vehicle to deliver this is how to connect mobile device information with real world behaviour.

For Ant Financial Group, for example, AI supports key business, like payment experience, targeted marketing, smart recommendations and anti-fraud and risk management. The scale of data processing is enormous, creating 2000 terabyte of data every day. Some of its services it has successfully monetised. For instance, offering user to pay $0.32 (RMB2) for real-time risk management service. The company also utilised machine-learning technology to launch an image-recognition system to aid vehicle insurance claims, an innovation between Alipay and China Taiping Insurance. On Singles Day 2017, it was reported that Alibaba used AI to generate 400 million customised banner advertisements in the month leading up to the shopping day. And at Taobao, Alibaba’s third-party ecommerce platform, users can already search by image.. Ant believes automated customer service has a higher satisfaction rate than humans. And it is using IoT on improving shopping such as payment method without mobile phones for transit and improving the experience of check in check out without mobile phone.

Another digital retail financial services provider looks at behavioural data such as transactional data, customers’ behaviours on the phone, the choices they make in their spending and social data. They found that people who apply for a loan between 1:00 and 6:00 am, for instance, are the highest risk. Additionally, the probability of default for someone who knows another bad borrower is nine times higher than an average borrower. Using these and other factors, they started understanding trends and behaviour. Rather than using Facebook advertising, the provider does gamification of social data on Facebook by telling customers to cooperate with them to individualise interest rates.

Assessment Methodology

The Best Digital Retail Financial Services Ranking is predicated by the core believe that an outstanding digital institution in retail financial services demonstrates the same long-term sustainable franchise as any other financial institution, based on a strong focus on the customer and a commitment to provide a frictionless customer experience, backed by innovative business processes and potentially new transformative technologies. We recognise digital financial institutions for their vision, execution and market transforming propositions that can make a real impact to its business, customers and the industry at large.

The assessment covered 9 commercial banks, 5 platform based ecosystems, 15 digital banks and 4 technology companies. The survey was undertaken between January and March 2018 and is based on The Asian Banker proprietary scorecard methodology.

The list of digital retail financial services institutions aimed to include the top digital retail financial services provider for each of the markets covered but does no claim to be exhaustive in regards to the ranking. Among the current top 10, WeLab and CreditEase are not included.

The following are the evaluating factors that we look at and the percentage we give to each of them:

.png)

.webp)