Rankings

Nov 23

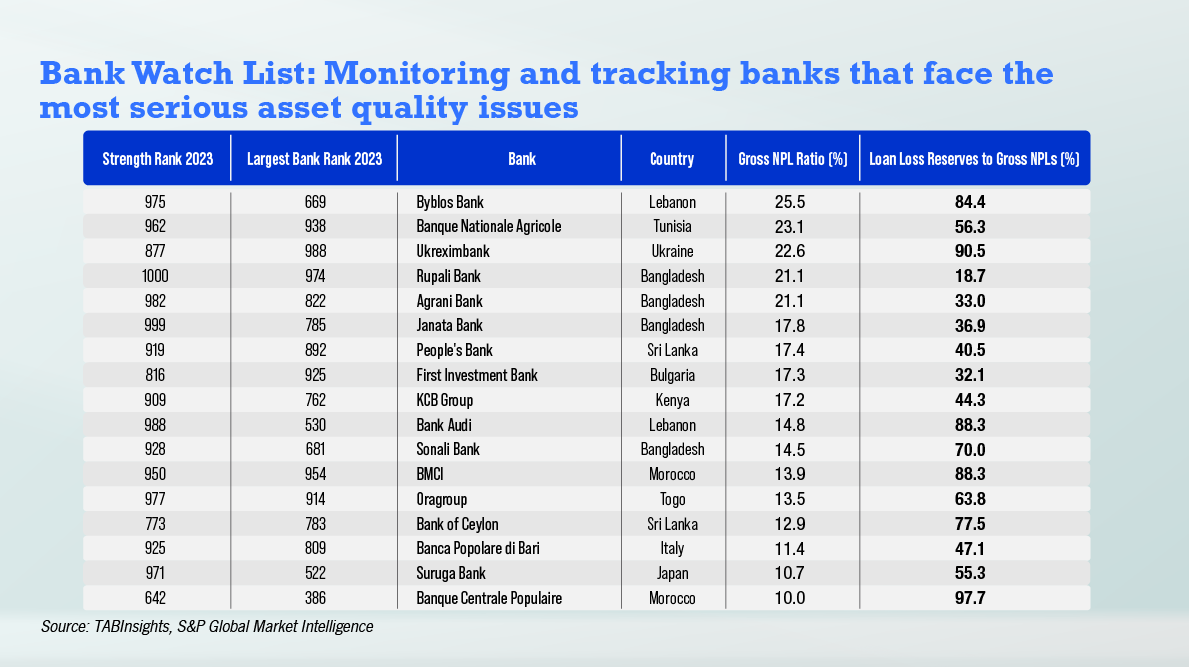

Four banks in Bangladesh on the TABInsights Bank Watch List reported an average gross NPL ratio of 17.8% in FY2022, while Indian banks demonstrated improved asset quality, with none making the list, highlighting resilience to economic fluctuations

.webp)