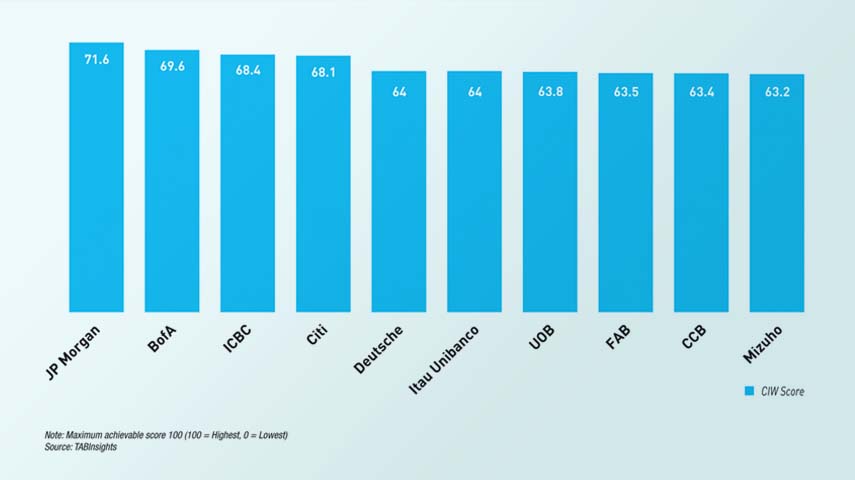

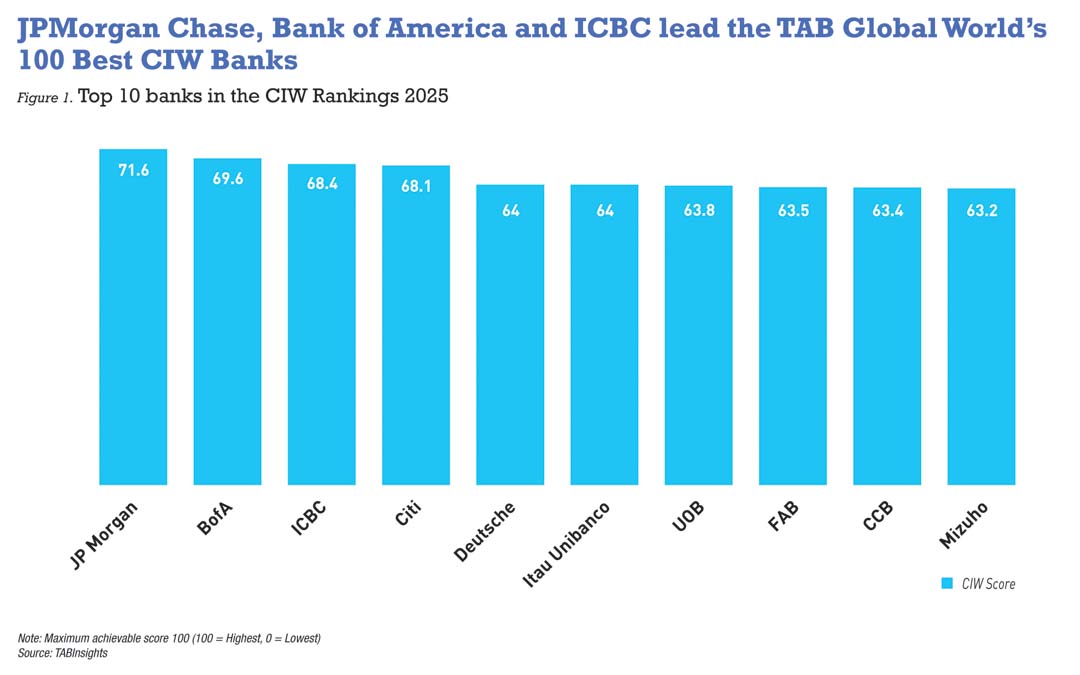

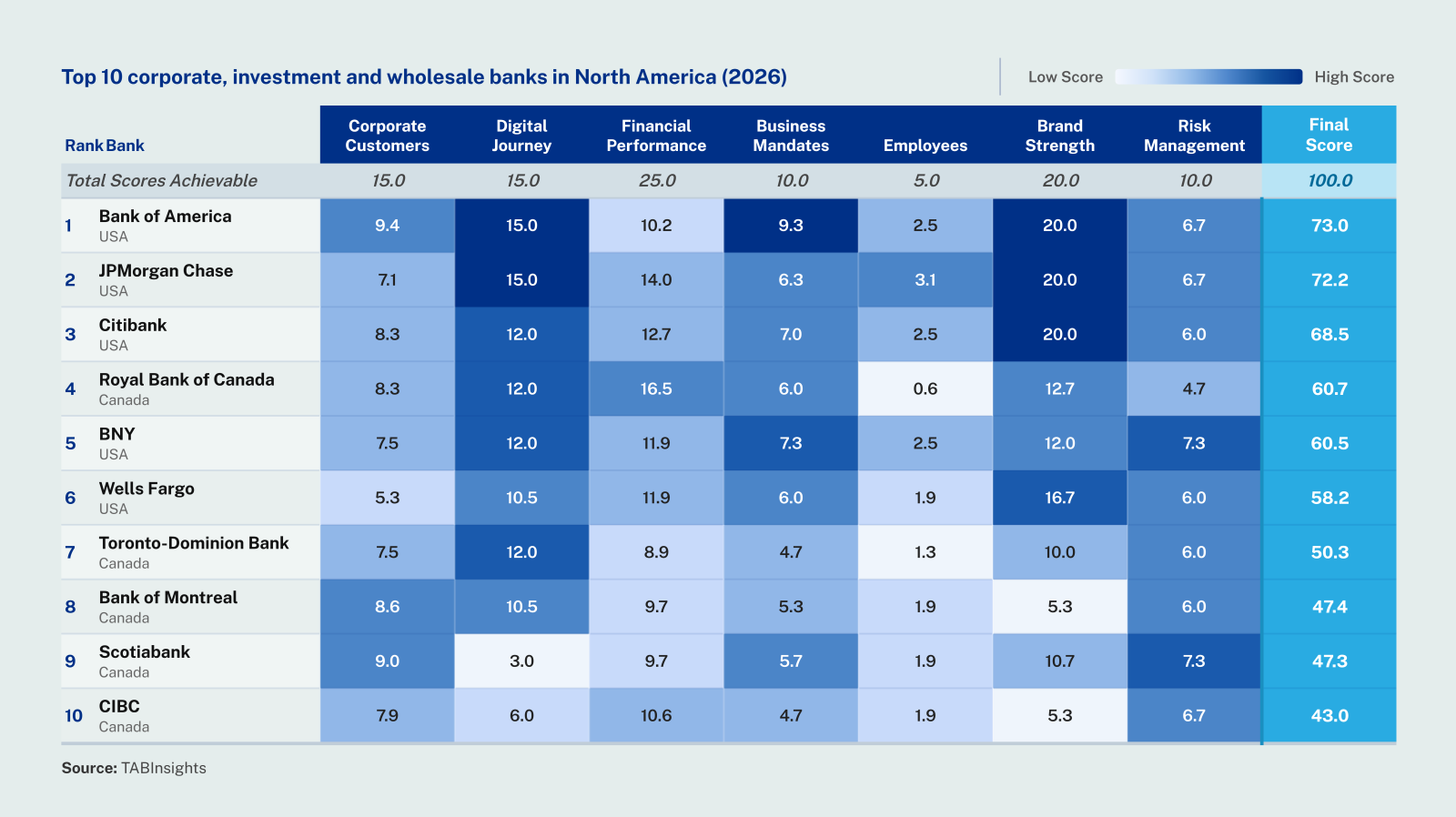

JPMorgan Chase, Bank of America, and Industrial and Commercial Bank of China (ICBC) topped the TAB Global World’s 100 Best Corporate, Investment and Wholesale (CIW) Banks Ranking 2025. Their dominance reflects a combination of balance sheet strength, global reach and product breadth. JPMorgan’s CIW assets allow it to anchor corporate and investment relationships across geographies, while Bank of America leverages its vast client base and integrated digital platforms. ICBC, meanwhile, reinforces its position as Asia’s leading CIW bank by combining its large-scale corporate lending capacity with an expanding international presence.

Beyond these global leaders, regional champions such as UOB, First Abu Dhabi Bank, and Bank Mandiri demonstrate alternative routes to success. Their strength lies in focused CIW asset strategies, rapid digital adoption, and superior cost discipline, proving that structural efficiency can rival absolute size in shaping market leadership.

The ranking covers 100 banks from 34 countries and jurisdictions, with CIW revenues ranging from $160 million to $70 billion and pre-tax return on assets (ROA) between 0.1% and 6.8%. Collectively, these institutions generated approximately $1.1 trillion in CIW revenue in FY2024, equivalent to 46% of their total income. The ranking is underpinned by a regression analysis that models each bank’s rankings as the dependent variable, with key performance indicators (KPIs) across seven dimensions: corporate customers, digital adoption, financial performance, business mandates, employees, brand strength, and risk management as the independent variables.

Assets, digital adoption and product breadth drive CIW leadership

The top 10 banks in the ranking are JPMorgan Chase, Bank of America, ICBC, Citi, Deutsche Bank, Itaú Unibanco, United Overseas Bank (UOB), First Abu Dhabi Bank (FAB), China Construction Bank, and Mizuho Bank. This group illustrates the diverse paths to success in global CIW banking. JPMorgan Chase, Bank of America, and Citi leverage their extensive scale and global networks, while Itaú Unibanco, UOB, and FAB demonstrate the power of regional dominance and superior efficiency. Chinese banks ICBC and CCB benefit from massive domestic scale, and Deutsche Bank and Mizuho Bank are refining strategies around core strengths in Europe and Asia, respectively.

Ranking results reveal that digital adoption, dedicated CIW assets, product breadth and geographic presence are the strongest predictors of a high score, followed by profitability and efficiency. Among these, digital capability emerges as the most critical differentiator. Banks in the top quartile report an average of 85% digitally active customers, compared with 59% in the bottom quartile. UOB, which ranked 7th, shows high digital engagement with 96% customer adoption, supporting efficiency.

The scale of a bank’s dedicated CIW assets is another primary indicator of its capacity to serve large corporate and institutional customers. The top three banks demonstrate balance sheet strength, with ICBC at $2.67 trillion, China Construction Bank at $2.34 trillion, and JPMorgan Chase at $1.77 trillion in CIW assets. However, the rankings show that focused scale can be equally effective.?Standard Bank of South Africa, ranked 34th, manages $103 billion in CIW assets yet dominates its region, supported by a strong ROA of 2.4%.

Finally, product breadth and market coverage adds another layer of advantage. Global institutions such as JPMorgan Chase, with 11 transaction banking products across more than 160 markets, and Standard Chartered, with 11 products in 70 markets, compete through comprehensiveness. By contrast, UOB and OCBC, each offering 10 products across 19 markets, prove that deep regional integration within ASEAN can rival global reach. This shows that both wide global networks and concentrated regional strategies can provide a winning formula for CIW banking.

Regional champions leverage digital platforms and customer depth

The TAB Global World’s Best 100 CIW Banks ranking, once limited to the top 50 banks, has been expanded to include banks from developed and emerging markets alike. The following regional champions, newly added to the ranking, illustrate how banks are driving CIW performance across multiple dimensions.

In Indonesia, Bank Mandiri consolidated its leadership anchored by digital engagement and wholesale banking. Its digital strategy underpinned customer engagement, with 29.3 million digitally active users on the Livin’ by Mandiri app, which processed 3.9 billion transactions over 2024. On the wholesale side, the Kopra by Mandiri platform supported corporate customers with transactions worth $1.43 trillion. Wholesale banking contributed 18.2% of the bank’s total revenue, reinforcing its importance within the group.

Across the Malacca Strait, Maybank led Malaysia’s CIW market, serving around 15,000 corporate customers. Wholesale banking accounted for 29.1% of total revenue in FY2024, underlining its central role in group earnings. The bank advanced its digitalisation push with 46.3% of customers now active online. Its integrated transaction banking, treasury and regional services strengthened its position as a facilitator of trade and investment across ASEAN.

In northern Europe, Nordea Bank remained the best CIW player in Finland, with operations extending across Sweden, Norway and Denmark. The bank delivered a return on equity of 16.7% in FY2024, while digital adoption was clear with more than 5.2 million customers active online and over 1.5 billion digital logins. Wholesale banking contributed 19.2% of the group’s revenue, complemented by $198.5 billion in sustainable financing over three years, cementing its role as both a digital and ESG-driven leader.

In Denmark, Danske Bank derived nearly a third of its revenue, 30.8%, from CIW banking. Its corporate business generated $1.4 billion in profit before tax in FY2024. The bank advanced its Forward ’28 strategy, enhancing its District digital platform for business customers and launching the “Become a customer” app, which streamlined onboarding and enhanced efficiency in corporate and institutional banking.

Further west, Bank of Ireland led the CIW sector domestically, serving 22,000 corporate customers. CIW operations contributed 42.1% of total revenue in FY2024, highlighting the segment’s importance within the bank’s model. Its trade finance offering stood out for combining a fully integrated digital platform with personalised advisory. By supporting importers and exporters with letters of credit, guarantees and collections, the bank enabled faster, safer and more efficient cross-border transactions.

Together, these banks illustrate how regional leaders are combining digitalisation, customer platforms and sector-specific offerings to anchor CIW banking as a key driver of performance.

Profitability and efficiency support, but don’t define, leadership

The financial performance of the best 100 banks reveals that while profitability and efficiency are essential for business health, they do not directly determine a bank’s CIW strength. Analysis shows no significant correlation between a bank’s rankings and its CIR or ROA. Instead, elite ranking status can be achieved by banks with widely varying financial profiles, where factors such as scale, digital maturity and market reach often offset or even justify moderate efficiency and profitability, highlighting the multifaceted nature of CIW banking leadership.

High-efficiency banks leverage exceptional cost discipline to support their standing: Emirates NBD leads with a CIR of 10.5%, while First Abu Dhabi Bank and Saudi National Bank maintain CIRs below 15%, translating into solid ROAs of 2.7%, 2.2%, and 2.2%, respectively, demonstrating how lean operations underpin profitability. High-profitability banks, such as ICICI Bank with ROA of 4.4% and Bank Central Asia with ROA of 4.9%, achieve standout returns but often rank outside the top tier, reflecting a trade-off with global scale.

Meanwhile, global-scale banks like JPMorgan Chase and ICBC maintain top positions despite moderate efficiency and returns, driven by dominant segment assets, product breadth and market presence. Together, these patterns indicate that TAB Global’s CIW rankings reward strategic balance across efficiency, profitability, and scale, rather than any single metric.

Expanding the ranking to 100 institutions highlights sharper contrasts in CIW performance. For instance, Bank Central Asia, with a 4.9% ROA, sits alongside Japan’s Mizuho at 0.4%, underscoring the diversity of successful business models. This broader scope provides deeper insight into how different strategies — whether regional dominance, global scale or operational efficiency — drive CIW leadership, confirming that top ranking is not solely determined by profitability or efficiency, but by alignment between financial performance and strategic focus.

.png)

.webp)